|

Position

|

NAME OF CANDIDATE

|

Votes

|

|

1

|

40. SAVLA PRITI PARAS- (MUMBAI)

|

1800

|

|

2

|

12. CHITALE SUSHRUT MUKUND- (MUMBAI)

|

1744

|

|

3

|

29. KHANDELWAL PURUSHOTTAM LAL- (AHMEDABAD)

|

1728

|

|

4

|

14. DESAI DRUSHTI RAHUL- (MUMBAI)

|

1642

|

|

5

|

8. ALSHI RAKESH GANPAT- (MUMBAI)

|

1630

|

|

6

|

46. TALATI ANIKET SUNIL- (AHMEDABAD)

|

1469

|

|

7

|

17. GADIA MANISH R- (MUMBAI)

|

1424

|

|

8

|

5. AGRAWAL PRADEEP KANAIYALAL- (VADODARA)

|

1344

|

|

9

|

28. KELKAR ABHIJIT JAYANT- (NAGPUR)

|

1331

|

|

10

|

44. SHARMA UMESH RAMNARAYAN- (AURANGABAD)

|

1241

|

|

11

|

37. SABOO KAMLESH- (THANE)

|

1170

|

|

12

|

42. SHAH PRIYAM RAMESHBHAI- (AHMEDABAD)

|

1114

|

|

13

|

34. MUNDADA SATYANARAYAN GOVERDHANLAL- (PUNE)

|

1078

|

|

14

|

3. AGARWAL VISHNU KUMAR - (MUMBAI)

|

1018

|

|

15

|

41. SHAH HARDIK PRAVINKUMAR- (SURAT)

|

1004

|

|

16

|

22. JAIN SANDEEP KAILASHCHAND- (MUMBAI)

|

949

|

|

17

|

30. KULKARNI VIKRANT MURLIDHAR- (NASHIK)

|

926

|

|

18

|

47. VAIDYA AMBARISH ASHOK- (PUNE)

|

891

|

|

19

|

23. JOSHI SARVESH NANDLAL- (PUNE)

|

842

|

|

20

|

25. KALA JAYESH UMEDMAL- (MUMBAI)

|

810

|

|

21

|

32. MAJITHIA NEEL PANKAJ- (MUMBAI)

|

798

|

|

22

|

9. BAJAJ LALIT LAXMINARAYAN- (MUMBAI)

|

788

|

|

23

|

1. AGARWAL BALKISHAN - (SURAT)

|

782

|

|

24

|

33. MEHENDALE KEDAR ACHYUT- (MUMBAI)

|

741

|

|

25

|

45. SHINAGARE SHILPA BABASAHEB- (MUMBAI)

|

733

|

|

26

|

24. KACHWALA MURTUZA ONALI- (KALYAN)

|

670

|

|

27

|

10. BARMECHA MOHANLAL SAMPATLAL- (AHMEDNAGAR)

|

662

|

|

28

|

27. KEDIA SUBODHKUMAR BAJRANGLAL- (AHMEDABAD)

|

647

|

|

29

|

43. SHAH SHRUTI JAYESH - (MUMBAI)

|

642

|

|

30

|

11. BHUTWALA HAREKRUSHNA BALVANTRAI- (SURAT)

|

583

|

|

31

|

36. PALIWAL DAYARAM- (MUMBAI)

|

582

|

|

32

|

16. DODHIA VANDANA VERSHIBHAI- (MUMBAI)

|

517

|

|

33

|

20. JAIN ASHOK CHAND- (MUMBAI)

|

484

|

|

34

|

31. LELE PRAMOD VISHNU- (THANE)

|

473

|

|

35

|

7. AGRAWAL VIMAL KUMAR- (MUMBAI)

|

439

|

|

36

|

4. AGRAWAL ASHWINI SURESH - (NAGPUR)

|

428

|

|

37

|

18. GANDHI PREMAL HEMANT- (MUMBAI)

|

424

|

|

38

|

21. JAIN MAHAVIR SHANTILAL- (THANE)

|

409

|

|

39

|

38. SANGHAVI ANKIT PANKAJ- (MUMBAI)

|

380

|

|

40

|

39. SARDA SATISH GIRDHARLAL- (NAGPUR)

|

380

|

|

41

|

2. AGARWAL MANOJKUMAR BABULAL - (PIMPRI)

|

356

|

|

42

|

15. DHAKER GOPAL- (MUMBAI)

|

308

|

|

43

|

26. KASLIWAL AMBAR- (MUMBAI)

|

287

|

|

44

|

6. AGRAWAL SWAPNIL MUKUND - (NAGAPUR)

|

272

|

|

45

|

35. MUNDADE BIPEEN GOPALDAS- (MUMBAI)

|

268

|

|

46

|

49. WARTY SHANTESH ARVIND- (MUMBAI)

|

242

|

|

47

|

13. DEHERKAR ARUN VASANT- (THANE)

|

87

|

|

48

|

48. VORA JAYESH SURYAKANT- (MUMBAI)

|

62

|

|

49

|

19. JAIN ARUN LAXMICHAND- (MUMBAI)

|

46

|

22 December 2015

RCM First preferences

Count down begins

Now the count down. The real numbers. What we see is guesses. And this all will answer the questions...

1. Can Gujarat give 3 CCM?

2. Can Julfesh Shah make it?

3. Who will be in Dhiraj Khandelwal or BM Agarwal

21 December 2015

Here is the list of sure shots in Central Council

Distribution of votes is still on. Looking at the current trend, here is the list of favorite contestants who seems to have taken a decisive lead.

Please note, this is based on the estimates on the votes in their tray:

1. Nilesh Vikamsey

2. S B Zaware

3. Jay chhaira

4. Dhinal Shah

5. Nihar Jambusariya

Please note, this is based on the estimates on the votes in their tray:

1. Nilesh Vikamsey

2. S B Zaware

3. Jay chhaira

4. Dhinal Shah

5. Nihar Jambusariya

ICAI Elections:NC Hegde and Purushottam Khandelwal

N C Hegde and Purushottam Khandelwal are doing exceptionally well this time. NC has has bounced back and Purushottam Khandelwal is getting flood of votes

ICAI Elections!!

Apologies my CA friends I am in Dubai and couldn't cover the elections this time and couldn't write the blog. I wish all the best to all the candidates.

26 September 2015

Relaxation of Additional Fees

Relaxation of additional fees and extension of last date of filing of for ms M GT-7 (Annual Retur n) and AOC-4 (Financial Statement). Looking to the delay in notification of the electronic versions of forms AOC-4, AOC-4 (XBRL), MGT-7 and AOC-4 CFS, the MCA has decided to relax the additional fees payable on forms AOC-4, AOC-4 XBRL and MGT-7 up to 31/10/2015. Further, a Company which is not required to file its financial statement in XBRL format and required to file its CFS (Consolidated Financial Statements) would be able to do so in the separate form for CFS without any additional fees up to 30/11/2015. [F. No. 1/34/2013-CL-V dated 13th July, 2015]

MCA Annual filing available wef 25-09-2015

MCA to make Annual filing forms available w.e.f. 25th September, 2015

New Versions of forms CRA-4 and CHG-4 are also likely to be modified w.e.f 25th Sept 2015.

Stakeholders are requested to plan accordingly.

25 September 2015

Summary of the moves for the Extention of Date u/s 44AB:-

Summary of the moves for the Extention of Date u/s 44AB:-

1.Bombay HC-Chamber of Tax Consultants Vs. Union of India & Ors (WP-2764/2015)

Adjourned to 29-09-2015

2. Orissa HC-Jagdish Prasad Mittal Vs. Union of India & Ors

WP-17178/2015

Adjourned to 25-09-2015

3. Karnataka HC-Karnataka State Chartered Accountants Association (KSCAA) Vs. Union of India & Ors

WP-41109/2015

Judgment on 28-09-2015

4. Rajasthan HC-Devendra Kumar Somani Vs. Union of India & Ors

(CW-10974/2015)

Now Listed on 29-09-2015

5.Delhi HC- Avinash Gupta & Ors. Vs. Union of India & Ors

(WP(C)-9032/2015)

Extension Refused :21-09-2015

6. Punjab & Haryana HC-Vishal Garg & Ors. Vs. Union of India & Anr (CWP-19770/2015)

Next Hearing : 28-09-2015

7.Gujarat HC-All Gujarat Federation of Tax Consultants (AGFTC) vs Central Board of Direct Taxes ( SCA-15075/2015)

Next hearing 28-09-2015.

24 September 2015

HC dismisses petition for extension

HC dismisses petition filed by Chartered Accountant seeking extension of tax audit due date; Petitioner argued that assessees are entitled as a matter of 'right', to 180 days period for filing of return which in the instant case was being denied since the forms were notified only on July 29, 2015; Petitioner further justified extension plea on grounds of amendments in Companies Act, bonafide impression among CAs that there would be changes/modifications in Form 3CD due to Finance Act amendments and alleged discrimination by CBDT through its act of granting extension for July 31st due date but refusing to do the same for tax audit; HC, rejecting petitioner's submissions, observes that nowhere in the scheme of Income tax Act is 180 days assured to the assessee, holds".. the time taken in audit, which is variable, will be determinative of the time available thereafter for filing the ITR. The said audit is not dependent upon the prescription of the forms for report of the said audit and / or for filing of the ITR. " ; HC notes that the CBDT has applied its mind in the matter, cites its press release dated September 9 ruling out any extension of due date; Further rules that such policy decisions of Government ought not to be interfered by the Court, unless undue prejudice caused; However Court directs CBDT to ensure that the forms that are to be prescribed for the Audit Report/for filing ITR, are available as on April 1 of the assessment year unless there is a valid reason that ought to be recorded :Delhi High Court

16 September 2015

Various Legal Phrases Used in Law:-

1.Anything which you cannot do directly that you cannot do directly

2.Deeming fiction cannot be stretched beyonyd the purpose for which it is created

3.The words used in Law are not used for Nothing

4.To invoke Provision : To make use of particular provision

5.Ipso Facto: By this fact alone or because of this matter alone

6.'MAY' may be treated as 'SHALL' but 'SHALL' shall not be treated as 'MAY'

7.Tenable: Acceptable in law

8.Redundant Provision : Out of Force or Outdated Provision

9.Quasi : Almost Similar to

10.Quasi Criminal: Almost equal to criminal

11.Jurisprudence: Law relating to particular matter

12.Mensrea: Guilty Mind

13.Ibid: As printed earlier

14.Suo Moto: On its own

15.Prima Facie: On its face

16.Non est: What is not in existence / Non existing thing

17.Call in question: To challenge

18.De Nova: Completely New

19.Sine quo non: Most essential thing

20.Purposes of this Act: Proceeding mustbe pending

21.Reason to believe Vs Reason to suspect: Refer various caselaws

22.Derived from & attributable to: Derived from refers to direct connection with aparticular matter whereas attributable to refers to an indirect connection

23.Mutatis Mutandis: After making necessary changes as may be required

24.Discovery Vs Detection: Discovery is made by the assessee whereas detectionisdone by the Assessing Officer

25.To Quash: The process of cancelling the proceeding of Assessing Authorities byJudicial Authorities

26.So far as may be: To the extent possible

27.Travisity of Justice : A ridiculous interpretation of a very serious statement,making amockery of a very serious matter

28.To impugne : To challenge

29.Save as otherwise provided : Except tothe extent as oppositely provided

30.If one section is overriding the other section : Use Words "Not withstandinganything contained in ……

"31.If one section is superceded by the other section : Use words "Save as otherwiseprovided……….."32.Other provisions apply in General way:Use words "Without prejudice to theprovisions ……………..

"33.Reckoned : Recognised, Counted, Calculated

34.Doctrine of Merger: When an order passed by the lower authority is superceded bythe higher authority

35.Doctrine : Principle or saying in general acceptance

36.In Pari Material Pavi Causa: Same material, same content {Eg. Sec. 24B of ITAct,1922 is Pari Material with Sec. 159 of IT Act, 1961. In such a case a judgement givenin respect of section 24B would be valid in respect of sec. 159}

37.Per se : By itself

38.Cy Press : As near as possible

39.Tax is always charged, Interest is levied and Penalty is imposed40 Deductions are admissible, Relief is granted.

41.Return is always furnished, Assessment order is made / passed.

42.De hors : Independent of

43.Order of Injunction of HC : Stay order.

44.Several Liability means separate liability. [Refer sections 168(3), 171(7), 179(1)178(5) & 188A.]

45.Legatee is a person for whose benefit there exists an asset of a deceased

46.Locus Standi : Directly involved in relation or deal.

47.Garnishee Proceeding : The proceeding which gives Govt. the right to attach (i.e.forcibly take over) any asset from a person who is defaulter.

48.Vitiate Proceedings : To make proceedings null, void.

49.Inter alia : Among other things.

50.Audit Altream partem : It is a principle of natural justice. According to this principle,which is the principle in every civilized jurisprudence, a person against whom anyaction is sought to be taken or a person whose rights or interests are to be affectedshould be given a reasonable opportunityto defend himself.

51.Resjudicata : [Once the decision of HC comes then on that same point again appealcannot be made.] The issue of Law whichhas been already decided shall not bepleaded for review.

52.In Limine : At the outset (i.e. at the beginning)

53.Suspended animus : An order under Appeal is not subject to any action by anyauthority till the order disposing of the appeal is available.

54.Subjudice : Under an appeal to a court,decision awaited.

55.Adjudicate : Consider for judgement. Acourt adjudicates means gives its decision ona particular matter.

56. Akin : Similar to; of the same typeCoterminus : Similar to; of the same type

57.Impediment : Obstacles or Hindrance.

58.Sine Di: For indefinite period.

59. To deduce : Logically come to the conclusion.

60.Purview : Scope

61.Bounty : Additional Advantage

62.Ad Hoc : Without any particular rate, percentage, proportion.

63.Ad infinitum : Without any Time limit.

64.Ad interim : In the Mean Time

65.Bonafide : Genuine

66.Surmises : Presumptions, own assumptions

67.Defacto : Infact

68.Defjure : In Law, irrespective of whatever the facts.

69.Ejusdem Generis : Of the same kind

70.Ex-gratia : As a matter of grace ir favour

71.Ignorantia Legis known excusat : Ignorance of law is not excused

72.Mesne Profit : Profit earned by somebody by wrongful possession of property.

73.Modus Operandi : Mode of Operation /Manner of working

74.Nexus : Close connection link.

75.Onus probandi : Onus of proof / The burden of Proof.

76.Non obnstante clause : That provisionhas superceding effect on any other provision

77. Raison D'etre : Reason or justification for existence.

78.Ratio Decidendi : Reason for deciding / Grounds for decision

79.Suijuris : of his own right.

80.Assessee engaged in ……………. : The activity should have started

81.Option Vs Discretion : Whenever choices is available to the assessee in respect ofany matter. Law uses the word at his option - for eg:1. Sec 11(11) - Explanation to Sec. 11 (1)2. Sec. 23(4)

82.amicus curiae : Friend of court; one who voluntarily or on invitation of the court, andnot on instructions of any party, helps thecourt in any judicial proceedings

83.audi alteram : hear the other side. Both sides should be heard before a decision isarrived at

84.caveat emptor : let the purchaser beware. A ---------- implying that the buyer mustbe cautious, as the risk is his and not thatof the seller.

85.cestui que trust : a beneficiary under atrust, the person for whose benefit the trust iscreated

86.ex officio : by virtue of an office.

87.ex parte : exkpression used to signify something done or said by one person not in thepresence of his opponent.

88.fait accompli : An accomplished act.

89.obiter diccum : an opinion of law not necessary to the decision. An exspression ofopinion (formed) by a judge on a question immaterial to the ratio decidendi, andunnecessary for the decision of the particular case. It is no way binding on any court,but may receive attention as being an opinion of the high authority.

90.pendente lite : during litigation.

91. per incuriam : through carelessness, through inadvertence. A decision of the court isnot binding precedent if given peer incuriam, that is, without the court's attention havingbeen drawn to the relevant authorities, or statutes.

92. pro tanto : to that extent, for so much, for as much as may be.

93. quid pro quo : the giving of one thing of value for another thing of value; one fortheother; thing given as compensation.

94. Ratio Decidendi : Reason for deciding / Grounds for decision

95. res integra : an untouched matter; a point without a precedent; a case of novelimpression.

96 rule njsi : a rule to show cause why a party should not do a certain act, or why theobject of the rule should not be enforced.

97 in personam : against the person; an act or preceeding done or directed withreference to no specific person or with reference to all whom it might concern.

98 in rem : an act / proceeding done or directed with reference to no specific person orwith refernce to all whom it might concern.

99 inter vivos : between living persons.

100 intestate : a person is deemed to die intestate in respect of property of which he or shehas not made a testamentary disposition ("will") capable of taking effect.

101 intra vires : within the powers; within the authority given by law.

102 ipse dixit : he himself said it; there is no other authority.

103 ipso jure : by the law itself ; by the mere operation of law.

104 lis pendens : a pending suit.

105 rule absolute : when, having heard counsels, court directs the performance of that actforthwith.

106 sine die : without delay.

107 stare decisis : to stand by things decided; to abide by precedents where the samepoints come again in litigation.

108 status quo : existing condition.

109 sub judice : before a judge or court; pending decision of a competent court.

110 ultra vires : beyond one's power..

Various Legal Phrases Used in Law:-

1.Anything which you cannot do directly that you cannot do directly

2.Deeming fiction cannot be stretched beyonyd the purpose for which it is created

3.The words used in Law are not used for Nothing

4.To invoke Provision : To make use of particular provision

5.Ipso Facto: By this fact alone or because of this matter alone

6.'MAY' may be treated as 'SHALL' but 'SHALL' shall not be treated as 'MAY'

7.Tenable: Acceptable in law

8.Redundant Provision : Out of Force or Outdated Provision

9.Quasi : Almost Similar to

10.Quasi Criminal: Almost equal to criminal

11.Jurisprudence: Law relating to particular matter

12.Mensrea: Guilty Mind

13.Ibid: As printed earlier

14.Suo Moto: On its own

15.Prima Facie: On its face

16.Non est: What is not in existence / Non existing thing

17.Call in question: To challenge

18.De Nova: Completely New

19.Sine quo non: Most essential thing

20.Purposes of this Act: Proceeding mustbe pending

21.Reason to believe Vs Reason to suspect: Refer various caselaws

22.Derived from & attributable to: Derived from refers to direct connection with aparticular matter whereas attributable to refers to an indirect connection

23.Mutatis Mutandis: After making necessary changes as may be required

24.Discovery Vs Detection: Discovery is made by the assessee whereas detectionisdone by the Assessing Officer

25.To Quash: The process of cancelling the proceeding of Assessing Authorities byJudicial Authorities

26.So far as may be: To the extent possible

27.Travisity of Justice : A ridiculous interpretation of a very serious statement,making amockery of a very serious matter

28.To impugne : To challenge

29.Save as otherwise provided : Except tothe extent as oppositely provided

30.If one section is overriding the other section : Use Words "Not withstandinganything contained in ……

"31.If one section is superceded by the other section : Use words "Save as otherwiseprovided……….."32.Other provisions apply in General way:Use words "Without prejudice to theprovisions ……………..

"33.Reckoned : Recognised, Counted, Calculated

34.Doctrine of Merger: When an order passed by the lower authority is superceded bythe higher authority

35.Doctrine : Principle or saying in general acceptance

36.In Pari Material Pavi Causa: Same material, same content {Eg. Sec. 24B of ITAct,1922 is Pari Material with Sec. 159 of IT Act, 1961. In such a case a judgement givenin respect of section 24B would be valid in respect of sec. 159}

37.Per se : By itself

38.Cy Press : As near as possible

39.Tax is always charged, Interest is levied and Penalty is imposed40 Deductions are admissible, Relief is granted.

41.Return is always furnished, Assessment order is made / passed.

42.De hors : Independent of

43.Order of Injunction of HC : Stay order.

44.Several Liability means separate liability. [Refer sections 168(3), 171(7), 179(1)178(5) & 188A.]

45.Legatee is a person for whose benefit there exists an asset of a deceased

46.Locus Standi : Directly involved in relation or deal.

47.Garnishee Proceeding : The proceeding which gives Govt. the right to attach (i.e.forcibly take over) any asset from a person who is defaulter.

48.Vitiate Proceedings : To make proceedings null, void.

49.Inter alia : Among other things.

50.Audit Altream partem : It is a principle of natural justice. According to this principle,which is the principle in every civilized jurisprudence, a person against whom anyaction is sought to be taken or a person whose rights or interests are to be affectedshould be given a reasonable opportunityto defend himself.

51.Resjudicata : [Once the decision of HC comes then on that same point again appealcannot be made.] The issue of Law whichhas been already decided shall not bepleaded for review.

52.In Limine : At the outset (i.e. at the beginning)

53.Suspended animus : An order under Appeal is not subject to any action by anyauthority till the order disposing of the appeal is available.

54.Subjudice : Under an appeal to a court,decision awaited.

55.Adjudicate : Consider for judgement. Acourt adjudicates means gives its decision ona particular matter.

56. Akin : Similar to; of the same typeCoterminus : Similar to; of the same type

57.Impediment : Obstacles or Hindrance.

58.Sine Di: For indefinite period.

59. To deduce : Logically come to the conclusion.

60.Purview : Scope

61.Bounty : Additional Advantage

62.Ad Hoc : Without any particular rate, percentage, proportion.

63.Ad infinitum : Without any Time limit.

64.Ad interim : In the Mean Time

65.Bonafide : Genuine

66.Surmises : Presumptions, own assumptions

67.Defacto : Infact

68.Defjure : In Law, irrespective of whatever the facts.

69.Ejusdem Generis : Of the same kind

70.Ex-gratia : As a matter of grace ir favour

71.Ignorantia Legis known excusat : Ignorance of law is not excused

72.Mesne Profit : Profit earned by somebody by wrongful possession of property.

73.Modus Operandi : Mode of Operation /Manner of working

74.Nexus : Close connection link.

75.Onus probandi : Onus of proof / The burden of Proof.

76.Non obnstante clause : That provisionhas superceding effect on any other provision

77. Raison D'etre : Reason or justification for existence.

78.Ratio Decidendi : Reason for deciding / Grounds for decision

79.Suijuris : of his own right.

80.Assessee engaged in ……………. : The activity should have started

81.Option Vs Discretion : Whenever choices is available to the assessee in respect ofany matter. Law uses the word at his option - for eg:1. Sec 11(11) - Explanation to Sec. 11 (1)2. Sec. 23(4)

82.amicus curiae : Friend of court; one who voluntarily or on invitation of the court, andnot on instructions of any party, helps thecourt in any judicial proceedings

83.audi alteram : hear the other side. Both sides should be heard before a decision isarrived at

84.caveat emptor : let the purchaser beware. A ---------- implying that the buyer mustbe cautious, as the risk is his and not thatof the seller.

85.cestui que trust : a beneficiary under atrust, the person for whose benefit the trust iscreated

86.ex officio : by virtue of an office.

87.ex parte : exkpression used to signify something done or said by one person not in thepresence of his opponent.

88.fait accompli : An accomplished act.

89.obiter diccum : an opinion of law not necessary to the decision. An exspression ofopinion (formed) by a judge on a question immaterial to the ratio decidendi, andunnecessary for the decision of the particular case. It is no way binding on any court,but may receive attention as being an opinion of the high authority.

90.pendente lite : during litigation.

91. per incuriam : through carelessness, through inadvertence. A decision of the court isnot binding precedent if given peer incuriam, that is, without the court's attention havingbeen drawn to the relevant authorities, or statutes.

92. pro tanto : to that extent, for so much, for as much as may be.

93. quid pro quo : the giving of one thing of value for another thing of value; one fortheother; thing given as compensation.

94. Ratio Decidendi : Reason for deciding / Grounds for decision

95. res integra : an untouched matter; a point without a precedent; a case of novelimpression.

96 rule njsi : a rule to show cause why a party should not do a certain act, or why theobject of the rule should not be enforced.

97 in personam : against the person; an act or preceeding done or directed withreference to no specific person or with reference to all whom it might concern.

98 in rem : an act / proceeding done or directed with reference to no specific person orwith refernce to all whom it might concern.

99 inter vivos : between living persons.

100 intestate : a person is deemed to die intestate in respect of property of which he or shehas not made a testamentary disposition ("will") capable of taking effect.

101 intra vires : within the powers; within the authority given by law.

102 ipse dixit : he himself said it; there is no other authority.

103 ipso jure : by the law itself ; by the mere operation of law.

104 lis pendens : a pending suit.

105 rule absolute : when, having heard counsels, court directs the performance of that actforthwith.

106 sine die : without delay.

107 stare decisis : to stand by things decided; to abide by precedents where the samepoints come again in litigation.

108 status quo : existing condition.

109 sub judice : before a judge or court; pending decision of a competent court.

110 ultra vires : beyond one's power..

15 September 2015

IT Industry Based Jurisdiction

F.No.225/246/2014/ITA.II

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

New Delhi the September, 2015

OFFICE MEMORANDUM

Subject: Committee to study the feasibility of implementing 'Industry Based Jurisdiction' instead of prevailing 'Geographical Jurisdiction' in a phased manner-reg.

Board has constituted a Committee to examine the feasibility of implementing 'Industry Based Jurisdiction' in a phased manner instead of the prevailing 'Territorial Jurisdiction' as recommended by the Tax Administration Reform Commission ('TARC').

2. The composition of the Committee is as follows:

Sl No.

|

Name

|

Designation

| |

1

|

Ms Sunita Puri

|

Principal Commissioner of Income Tax -IV, Delhi

|

Committee In- charge

|

2

|

Sh. B. K. Singh

|

CIT(A)-11, Delhi

|

Members

|

3

|

Sh. Samar Bhadra

|

ADG (System)-3, Delhi

| |

4

|

Sh Rajeev Ranka

|

Add I. CIT (Audit-1), Delhi

| |

5

|

Sh. Rajesh Kedia

|

Addl CIT, Delhi

| |

6

|

Smt. Garima Bhagat

|

Addl CIT, Delhi

|

Member Secretary

|

3. The terms of reference of the Committee will be as follows:

(i) To carry out analysis of prevailing 'territorial jurisdiction' in Income Tax Department and study of its various aspects keeping in view the various responsibilities assigned and discharged by the Assessing officers who are located in more than 550 locations ranging from mofussil charges to metropolises.

(ii) Efficacy of existing dedicated Ranges dealing with cases of Trusts I AOP I Professionals I Industry specific jurisdiction (in some corporate charges) etc. may be analyzed with a view to examine the feasibility of implementing the same on all India basis in a phased manner.

4. The Committee may co-opt other members, as it deems fit to have proper representation, co-ordination and feedback from field formations in metro I non-metro I mofussil charges.

5. The Committee shall submit its report to Member (IT), CBDT by 15 th October, 2015.

6. The Headquarters of the Committee will be in Delhi.

This issues with the approval of the Chairperson, CBDT.

(Rohit Garg)

Deputy Secretary (ITA.II)

Deputy Secretary (ITA.II)

MCA Update on Deposit From Relative By Private Limited Company:

MCA Update on Deposit From Relative By Private Limited Company:

Deposits rules are quickly getting aligned with old 58A exempted rules to private limited company.

Without any upper limit of amount, now a private company can accept unsecured loans apart from director even from a relative (as per definition) of a director of the company with simple declaration saying the relative has not borrowed same from others. The relative need not be a shareholder of the company.

http://www.mca.gov.in/Ministry/pdf/Amendement_Rules_15092015.pdf

Deposits rules are quickly getting aligned with old 58A exempted rules to private limited company.

Without any upper limit of amount, now a private company can accept unsecured loans apart from director even from a relative (as per definition) of a director of the company with simple declaration saying the relative has not borrowed same from others. The relative need not be a shareholder of the company.

http://www.mca.gov.in/Ministry/pdf/Amendement_Rules_15092015.pdf

10 September 2015

Sovereign Gold Bonds Scheme

The government today approved the Sovereign Gold Bonds Scheme, which was announced in the Budget 2015-16. As investors will get returns that are linked to gold price, the scheme is expected to reduce the demand for physical gold. The bonds will offer same benefits as physical gold.

They can be used as collateral for loans and can be sold or traded on stock exchanges as they are available in demat form. At the same time investors need not worry about holding physical gold.

The gold bonds will be issued by the Reserve Bank of India. Since these are Government of India bonds, they are sovereign.

The bonds will be denominated in grams of gold. Investors can pay money and buy these bonds from intermediaries, who will be announced later.

* The bonds can be purchased only by resident individuals or entities. There will be a cap on bonds that can be purchased. It could be 500 gms per person per year.

* The government will decide the rate of interest. The rate will be calculated on the value of the gold at the time of investment. It could be floating or fixed rate. The principal amount of investment, which is denominated in grams of gold, will be redeemed at the price of gold at that time. If the price of gold has fallen from the time that the investment was made, the depositor will be given an option to roll over the bond for three or more years.

* The bonds will be available both in demat and paper form. They will be issued in denominations of 5,10,50,100 gms of gold or other denominations

* The bonds will be issued and redeemed by banks, non-banking finance companies, National Saving Certificate (NSC) agents for a fee. This fee will be decided later

* The price of gold may be taken from the reference rate, as decided and the rupee equivalent amount may be converted at the RBI reference rate on issue and redemption. This rate will be used for issuance, redemption and Loan to Value purpose and disbursement of loans.

* The tenor of the bond could be for a minimum of five to seven years.

* These bonds can be used as collateral for loans. The LTV will be equal to that of ordinary gold loans. As per RBI regulations, the maximum LTV allowed for gold loans is 75 per cent.

* It will be possible to sell and trade the bonds on exchanges, in case investors want to redeem them before maturity. The KYC for the bonds is same as that for gold. Currently, if you purchase gold worth more than Rs 50,000 you have to show proof of KYC, such as PAN card, etc.

* Capital gains tax will be the same as for physical gold for individual investors. This means that short-term capital gains tax will apply if you sell within three years. The profits will be added to your income and taxed at income slab. Long term capital gains tax is 20 per cent with indexation.

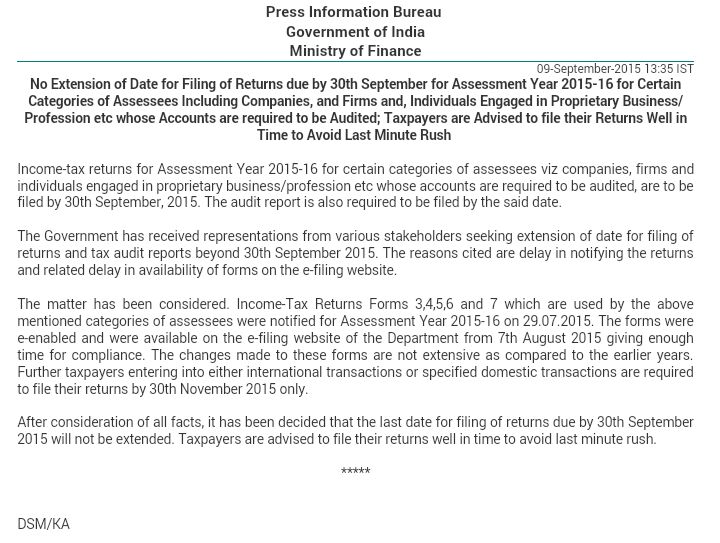

09 September 2015

t has been decided that the last date for filing of returns due by 30th September 2015 will not be extended.

Tweet by finance ministry:

It has been decided that the last date for filing of returns due by 30th September 2015 will not be extended.@arunjaitley #income #tax

Here is the pib release http://pib.nic.in/newsite/PrintRelease.aspx?relid=126732

It has been decided that the last date for filing of returns due by 30th September 2015 will not be extended.@arunjaitley #income #tax

Here is the pib release http://pib.nic.in/newsite/PrintRelease.aspx?relid=126732

08 September 2015

ITAT accedes to ICAI's plea

ITAT accedes to ICAI's plea in Miscellaneous Application to modify/review its order wherein the Tribunal had strongly criticized the Institute's functioning; Tribunal accepts ICAI's argument that that its observations in the original order about the CA profession and conduct of the students pursuing the CA courses, were not necessary to adjudicate the issues urged before it by the assessee; Clarifying that it was not the intention of the Tribunal to target any particular person or the ICAI, modifies para 9.6 of its original order that the Institute considered as "offensive"; ITAT in its original order, dismissed assessee's plea to condone a 2984 days delay in filing of appeal on grounds of 'improper advice' given by CA firm; While raising alarms over the reckless advice given by the CA firm, the Tribunal called on the ICAI to stem the"deteriorating standards" & "alarming practices" among some CAs; While modifying its order, Tribunal however reserves right to opine on important developments affecting the nation, observes “... the Income tax Appellate Tribunal, being a part of Government of India, should not shut its eyes when it is noticed that certain developments occurring in the Country may affect the Country as a whole, more particularly when the reputation of particular profession, from whom the Tribunal is getting assistance in the dispensation of justice, is at stake.”; Concludes that it would be incorrect to interpret that the Tribunal in its original order had commented upon the standards of CA profession or the ICAI, however as the said observations gave room for misinterpretation and thereafter resulted in controversies, replaces the same : Mumbai ITAT

The ruling was delivered by ITAT bench of Shri D. Manmohan and Shri B. R. Baskaran.

05 September 2015

Representation to CBDT and MCA

BCAS in its knowledge sharing mission, interacts with the law makers to bring clear, predictable, just, hassle free laws and good governance. In this endeavour, this month the Society has made 2 representations to the government on various issues and hardships faced by the Chartered Accountants.

a) Representation to CBDT on E-filing of Wealth-Tax Returns, and

b) Representation to the Ministry of Corporate Affairs for The Company Act, 2013 on issues arising from the implementation of the Companies Act, 2013.

We hope that this will help our members and their clients.

Please click on below links to read the full representations :

· Representation to CBDT on E-filing of Wealth-Tax Returns for A.Y. 2015-16

· The Companies Act 2013 - Issues arising from the implementation of the companies act, 2013

04 September 2015

27 FAQs on Black Money Law

CBDT- Highlights of 27 FAQs on Black-money law amnesty scheme and download circular

Highlights:

If a public limited company makes a declaration then Directors of the company will not get immunity against offence punishable under SEBI Act or under IPC.

In case of an e-wallet or virtual card account online which is normally maintained for playing online games, it is similar to a bank account where inward and outward cash movement takes place. A declaration can be made in the manner prescribed for a bank account.

Whether a valuation report is to be filed along with a Declaration of a foreign asset the CBDT clarified that it is not necessary but the declarant should keep such a document used for arriving at the value of the asset.

If a person has from time to time transferred funds from his account to the accounts of his spouse or child whether the spouse or the child is also required to make a declaration, the CBDT has clarified that it is not required if no fund has been deposited in their account in addition to the ones done by the person.

If an employee makes a declaration of asset made out of income received from his employer, the employer shall be deemed to be an assessee in default u/s 201(1) for non-deduction of TDS, the CBDT has clarified that once declaration is made by the employee, the employer will escape the rigour of TDS but not the interest element and also the penalty.

Whether if a partnership firm makes declaration of undisclosed assets, partners will earn the immunity, the CBDT has clarified that partners shall be eligible for the immunity promised under the Scheme.

The Act will not provide immunity against punishable offence under SEBI Act/ Regulations or under IPC where disclosure is made under Chapter VI of the Act.

In case where a private trust (which has also set up a company holding 100% shares) is created outside India by a settlor out of undisclosed income, valuation of shares of the company should be made first as per Rule 3(1)(c) and then the value of net assets of the trust shall be determined.

A declarant will not be required to explain details of entries in foreign bank account at the time of declaration but is only expected to provide broad computatio

02 September 2015

Shah Report on MAT

Government Accepts Shah Panel Report, MAT Not to be Levied on FIIs

Finance Minister Arun Jaitley on Tuesday announced that the government has accepted Justice AP Shah Panel's recommendations on not levying MAT on Foreign Institutional Investors.

A. Highlights of speech

Here are the highlights of his speech.

- Justice AP Shah Panel had submitted its report on MAT to government few weeks ago.

- Certain questions which were in the mind of the CBDT were put forth to the MAT committee.

- Justice AP Shah report on MAT to be made public soon.

- Shah panel gave recommendations regarding levy of MAT On FIIs prior To April 1, 2015.

- Have accepted the recommendations of the Justice Shah Panel on MAT.

- Hope to move amendment to Tax Act in winter session of Parliament or whenever the next session is.

- AP Shah report says MAT on capital gains made by FIIs was not applicable.

- What applies post April 2015, that is no MAT on capital gain on FIIs, will also apply on pre-April 2015.

B. Recommendations of AP Shah Pane Committee

In view of the findings and upon a considered deliberation, we would like to make the following recommendations to the Government:

(i) To bring an amendment to Section 115JB of the Income Tax Act, 1961 clarifying the complete inapplicability of the MAT provisions to FIIs/FPIs; or

(ii) CBDT may issue a circular clarifying the complete inapplicability of the MAT provisions to FIIs/FPIs.

01 September 2015

IT Scrutiny Guidelines-2015-16

Criteria for manual selection of scrutiny cases during FY 2015-16

CBDT Instruction No. 8 Dated 31-8-2015

Highlights:

Cases involving addition in excess of Rs. 10 lakhs in earlier assessment year and all search-seizure-survey and re-assessment cases to be picked up for compulsory manual scrutiny.

Cases where charitable trusts/institutions are claiming Sec 11/Sec 10(23C) exemption despite Sec 12AA registration /Sec 10(23C) approval denial also to be picked up for compulsory manual scrutiny.

By and large no substantial changes via-à-vis similar CBDT instruction issued last year.

31 August 2015

Amendment to Customs Duty Free Allowance

Notification No.76/2015

CBEC has made Custom Duty Free Allowance to Rs.45,000/- for passengers of Indian origin and foreigners of over 10 year of age residing in India.

Duty free limit of Indian Currency that can be brought in India has been increased from Rs.10,000 to Rs.25,000 in FORM 1

Due date for filling of Income Tax Returns has been extended form 31-8-2015 to 7-9-2015 for Gujarat State,

Due date for filling of Income Tax Returns has been extended form 31-8-2015 to 7-9-2015 for Gujarat State, vide CBDT Notification dtd: 31-8-2015.

28 August 2015

Dept Clarification on Restaurant Service (Home Delivery)

Chandigarh Service Tax Dept. clarifies that free home delivery / pick-up of food is not liable to service tax; States that dominant nature of transaction is that of 'sale' as food is not served at restaurant and no other element of service such as ambience, live entertainment (if any), air conditioning or personalised hospitality is offered; Clarifies, "Service Tax can be levied if there's an element of 'Service' involved which would typically be the case where food is served in restaurant." : Dept Clarification

SEBI Guidance Note on Insider Trading

SEBI issues Guidance Note on Insider Trading Regulations, clarifies on ESOPs & contra-trades

|

SEBI issues Guidance Note on Insider Trading Regulations, 2015; Clarifies that exercise of ESOPs shall not be considered to be "trading" except for the purposes of Chapter III (relating to 'disclosure of trading by insiders'); States that any derivative contract that is settled in cash on expiry shall be considered to be 'contra-trade' and the trading in index futures or such other derivatives where scrip is part of such derivatives, need not be reported; States that buy-back offers, open offers, rights issues, FPOs, bonus are available to designated persons, and 'contra-trade' restrictions shall not apply; Clarifies that pledgor / pledgee may demonstrate that creation of pledge or invocation of pledge was bona fide and prove their innocence under proviso to Reg. 4(1) of the Regulations (relating to 'Trading when in possession of unpublished price sensitive information'); With respect to the trades done by compliance officer, SEBI clarifies that board of directors of the company shall be the approving authority and may stipulate procedures as are deemed necessary for ensuring necessary compliances: SEBI

|

Amendment to Arbitration Law

Cabinet approves arbitration law amendments for expeditious case disposal, cost-effective arbitration

Union Cabinet approves amendments to arbitration law, with an aim to ensure neutrality of arbitrators, expeditious disposal of cases, making arbitration more user friendly & cost effective; Amendments include disqualification of arbitrator if he has any relationship or interest in the matter, insertion of a provision for fast track procedure for conducting arbitration; Also includes amendment to Section 34 relating to grounds for challenge of an arbitral award, to restrict the term "Public Policy of India" (as a ground for challenging the award) by explaining that only where making of award was induced or affected by fraud or corruption, or it is in contravention with the fundamental policy of Indian Law or is in conflict with the most basic notions of morality or justice, the award shall be treated as against Public Policy of India; Amendments seek insertion of a new provision that Arbitral Tribunal shall make its award within a period of 12 months and if the award is made within a period of six months, arbitrator may get additional fees if the parties so agree; New provision inserted to provide that application to challenge the award is to be disposed of by the Court within 1 year, thereby ensuring speedy disposal of cases; New Section 31A to be added for providing comprehensive provisions for costs regime, applicable both to arbitrators as well as related litigation in Court, that will avoid frivolous and meritless litigation/arbitration; Amendments also empower Arbitral tribunal to grant all kinds of interim measures which the Court is empowered to grant : Govt. Press Release

20 August 2015

ST Clarification on Section 73,76 & 78

F.No.137/46/2015-Service Tax

GOVERNMENT OF INDIA

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF EXCISE & CUSTOMS

SERVICE TAX WING

NEW DELHI

MINISTRY OF FINANCE

DEPARTMENT OF REVENUE

CENTRAL BOARD OF EXCISE & CUSTOMS

SERVICE TAX WING

NEW DELHI

Dated: August 18, 2015

To

All Principal Chief Commissioners of Central Excise

All Chief Commissioners of Central Excise/ Service Tax

Principal Directors General of Goods & Services Tax/ Systems/Central Excise Intelligence

Director General of Audit

All Principal Commissioners of Central Excise/Service Tax

All Commissioners of Central Excise/Service Tax

All Principal Commissioners/Commissioners LTU

Joint Secretary TRU-1/TRU-II/Review

Commissioner Central Excise/ Service Tax/Legal/PAC

All Chief Commissioners of Central Excise/ Service Tax

Principal Directors General of Goods & Services Tax/ Systems/Central Excise Intelligence

Director General of Audit

All Principal Commissioners of Central Excise/Service Tax

All Commissioners of Central Excise/Service Tax

All Principal Commissioners/Commissioners LTU

Joint Secretary TRU-1/TRU-II/Review

Commissioner Central Excise/ Service Tax/Legal/PAC

Subject: Clarification regarding the provisions of Section 73, 76 and 78 of the Finance Act, 1994 and Section 11AC of the Central Excise Act, 1944 after amendments made vide Finance Act. 2015

Consequent to the amendments made to section 73, 76 and 78 of the Finance Act, 1994 and section 11AC of the Central Excise Act, 1944, vide Finance Act, 2015 with effect from 14.05.2015, field formations have sought certain clarifications with regard to detections made during audit, investigation or scrutiny. Keeping in mind the need to reduce litigation as well as paperwork and compliance formalities. I am directed to convey the following clarifications.

2.0 Issuance of a Show Cause Notice (SCN)

Doubt: Does a SCN have to be issued in a case involving the extended period of limitation, where the assessee pays the tax/duty, interest and 15% penalty as prescribed?

2.1 In a case involving the extended period of limitation, if an assessee pays the service tax/central excise duty, interest and penalty equal to 15% of the tax/duty and makes a request in writing that a written SCN may not be issued to them, then in such cases the SCN can be oral and the representation (if he desires) against it also oral. In other words, an assessee can request for an informed waiver of a written SCN. The Supreme Court in the case of Commissioner of Customs, Mumbai versus Virgo Steels reported in 2002(141) E.L.T 598 (S. C.) has held that:

"14. From the ratio laid down by the Privy Council and followed by this Court in the above cited judgments, it is clear that even though a provision of law is mandatory in its operation if such provision is one which deals with the individual rights of person concerned and is for his benefit, the said person can always waive such a right.

15. Bearing in mind the above decided principle in law, if we consider the mandatory requirement of issuance of notice under Section 28 of the Act, it will be seen that that requirement is provided by the Statute solely for the benefit of the individual concerned, therefore, he can waive that right. In other words, this Section casts a duty on the Officer to issue notice to the person concerned of the proposed action to be taken. This is not in the nature of a public notice nor any person other than the person against whom the proceedings are initiated has any right for such a notice. Thus, the right of notice being personal to the person concerned the same can be waived by that person.

16. If the above position in law is correct, which we think it is. M/s Virgo Steels, having specifically waived its right for a notice, cannot now be permitted to turn around and contend that the proceedings initiated against them are void for want of notice under Section 28 of the Act, so as to frustrate the statutory duty of the Revenue to demand and collect customs duty which M/s Virgo Steels had intentionally evaded."

Although this decision is in relation to section 28 of the Customs Act, 1962. the principles laid down are equally applicable to SCNs issued under other statutes. Hence, an assessee can waive the requirement of a written SCN.

2.2 Further, section 124 of the Customs Act, 1962 provides, inter alia, that no order confiscating any goods or imposing any penalty on any person shall be made unless the owner of the goods or such person is given a notice in writing, an opportunity of making a representation in writing and a reasonable opportunity of being heard. The section also provides that the notice and the representation may, at the request of the person concerned, be oral. This provision has been made applicable to the Central Excise Act, 1944 vide notification number 68/63-Central Excise dated 04,05.1963 issued under section 12 of the Central Excise Act. 1944. The said section of the Central Excise Act is also applicable to service tax vide section 83 of the Finance Act, 1994.

2.3 If the grounds on which the department feels that there has been short/non-payment of tax/duty are intimated to the assessee orally with its quantification and the assessee indicates in writing that he has been informed about such grounds and he accepts the grounds and the quantification and is waiving the requirement of a written SCN, then a written SCN need not be issued.

2.4 Further, clause (i) of the second proviso to section 78 of the Finance Act, 1994 and clause (d) of sub-section (1) of section 11AC of the Central Excise Act. 1944 refer to a thirty day period, from the date of service of the notice, within which the assessee may make the payment of tax/duty, interest and reduced penalty of 15%. In case the assessee makes a written request for waiver of a written SCN, the thirty day period can be computed from the date of receipt of such a letter by the department.

2.5 There is no bar on an assessee making the payment of tax/duty, interest and reduced penalty of 15% even before the date of receipt of such a letter by the department. Such an assessee cannot be placed on a worse footing than one who pays tax/duty, interest and reduced penalty of 15% within 30 days of the receipt of the SCN/receipt of letter by the department.

3.0 Conclusion of proceedings

Doubt: Who is competent to order conclusion of proceedings if the conditions meriting conclusion of proceedings are fulfilled?

3.1 Conclusion of proceedings may be approved by an officer equal in rank to the officer who is competent to adjudicate such cases. The cases can be closed by officers of DGCEI/Executive Commissionerate/Audit Commissionerate, as the case may be. If multiple issues involving different monetary values arise from the same proceedings, then the sum total involved in all the issues arising from the same proceedings should be considered for conclusion of proceedings. The conclusion of proceedings should invariably be intimated to the assessee in writing. There is no need to issue an adjudication order. Further, there is no need to undertake review of such conclusion of proceedings.

3.2 It is further clarified that as per section 73(3) of the Finance Act, 1994, in cases not involving fraud, suppression of facts, etc, if the assessee pays the tax and interest thereon, on the basis of his own ascertainment or that ascertained by the department, no penalty is payable and no show cause notice shall be served under sub-section (1) of section 73 in respect of the amount so paid. Further, as per provisions of clause (i) of proviso to section 76, in such cases not involving fraud, suppression of facts, etc, if the tax and interest thereon is paid within 30 days of the issuance of SCN, no penalty shall be payable and the proceedings shall be deemed to be concluded. These two provisions have to be read harmoniously to conclude that in cases not involving fraud, suppression of facts, etc, if the assessee pays the tax along with interest, either within 30 days of issuance of SCN or before the issuance of SCN, then in such cases proceedings shall be deemed to be concluded. Legal provisions for similar closure in central excise are present in clause (a) of sub-section (1) of section 11 AC of the Central Excise Act, 1944.

(Himani Bhayana)

Under Secretary (Service Tax)

Under Secretary (Service Tax)

Subscribe to:

Posts (Atom)

-

*1. What is Pradhan Mantri Garib Kalyan Deposit Scheme (PMGKDS), 2016?* Pradhan Mantri Garib Kalyan Deposit Scheme (PMGKDS), 2016 is a sche...

-

Hello, This year I have seen a very large No। of mails from members who are not satisfied with the new norms of Bank Branch Audit Allotment,...

-

After the ICAI regional council and central council elections , there is an anxious waiting period for resul...