MCA notifies CARO, 2016, applicable for FY beginning on or after April 1, 2015

31 March 2016

25 March 2016

Inclusion of Interest Income in the Return of Income filed by Persons liable to Pay Tax

Press Information Bureau

Government of India

Ministry of Finance

23-March-2016 17:29 IST

Inclusion of Interest Income in the Return of Income filed by Persons liable to Pay Tax

Information regarding interest earned by individuals and business entities on term deposit is filed with the Income Tax Department by banks including co-operative banks and other financial institutions and State treasuries etc. Form 26AS reflects only those payments on which tax has been deducted and it can be viewed by the individual tax payer by logging in to www.incometaxindiaefiling.gov.in. The information about interest payments without deduction of tax is also filed by the payer with the Department.

Central Board of Direct Taxes(CBDT) hereby informs the persons earning interest income that interest credited/received on deposits is taxable unless exempt under Section 10 of the Income-tax Act. Such interest income should be shown in the return of income even in cases where Form 15G/15H has been filed if the earning is not exempt under Section 10 of the Income-tax Act and the total income of the person exceeds the maximum amount not chargeable to tax.

Tax payers are advised to collect correct details of interest received or credited and

· file their return of income for assessment year 2014-15 (if not filed already) on or before 31.03.2016 in case their total income exceeds the maximum amount not chargeable to tax.

· revise their return of income for assessment year 2014-15/2015-16 if the return already filed does not include taxable interest income.

· file return of income for assessment year 2015-16, if not filed so far by including taxable interest income if any, on or before 31.03.2016 and avoid penalty u/s 271F.

For more details, you may contact your Assessing Officer or Toll free number 1800-180-1961.

*************

DSM

Government of India

Ministry of Finance

23-March-2016 17:29 IST

Inclusion of Interest Income in the Return of Income filed by Persons liable to Pay Tax

Information regarding interest earned by individuals and business entities on term deposit is filed with the Income Tax Department by banks including co-operative banks and other financial institutions and State treasuries etc. Form 26AS reflects only those payments on which tax has been deducted and it can be viewed by the individual tax payer by logging in to www.incometaxindiaefiling.gov.in. The information about interest payments without deduction of tax is also filed by the payer with the Department.

Central Board of Direct Taxes(CBDT) hereby informs the persons earning interest income that interest credited/received on deposits is taxable unless exempt under Section 10 of the Income-tax Act. Such interest income should be shown in the return of income even in cases where Form 15G/15H has been filed if the earning is not exempt under Section 10 of the Income-tax Act and the total income of the person exceeds the maximum amount not chargeable to tax.

Tax payers are advised to collect correct details of interest received or credited and

· file their return of income for assessment year 2014-15 (if not filed already) on or before 31.03.2016 in case their total income exceeds the maximum amount not chargeable to tax.

· revise their return of income for assessment year 2014-15/2015-16 if the return already filed does not include taxable interest income.

· file return of income for assessment year 2015-16, if not filed so far by including taxable interest income if any, on or before 31.03.2016 and avoid penalty u/s 271F.

For more details, you may contact your Assessing Officer or Toll free number 1800-180-1961.

*************

DSM

22 March 2016

e Filing of Form 15H/G-Procedure

Step-wise Procedures and Guide for e-filing of Form 15G 15H by Deductors

Step-wise Procedures and Guide for e-filing of Form 15G 15H in electronic form by the deductors to the office of the income tax

CBDT vide notification No. 76/2015 dated 29/09/2015 provided for the electronic filing of form 15G and form 15H declarations by person claiming receipt of certain incomes without deduction of tax wef 01/10/2015.

Later Directorate of lncome-tax (Systems) vide Notification No. 04/2015 dated 01/12/2015 further specified the procedure , formats and standards facilitating electronic filing of the Form 15G and 15H.

Electronic formats have since been finalised and have been made live. Income Tax Department has also specified Instructions to e-File "Statement of Form 15G/15H which are reproduced here under together with added visuals to help users.

(A) Registration Process:

To electronically file the "Statement of Form 15G/15H", the user should hold a valid Tax Deduction Account Number (TAN) and should be registered at incometax e-filing website in the category as "Tax Deductor & Collector".

For Registration, go to registration page, select "Tax Deductor & Collector" and complete the registration process.

(B) Filing Process:

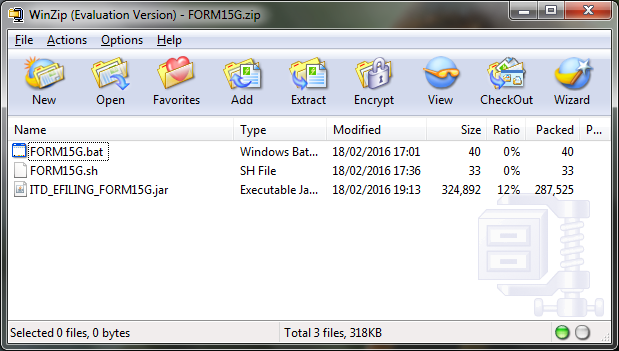

(1) Download FORM 15G/15H utility from Downloads page -> Forms (Other than ITR) -> FORM 15G/FORM 15H (Consolidated) in zip format

(2) Extract/un-zip the files into a folder and click on the ".bat" file to activate Form 15G/15H as the case may be

(3) Please note that the Form 15G and 15H utilities require the following pre-requisite platforms to run:

(i) Operating systems – Windows 7 or above, latest Linux or Mac OS 10.10(OS X Yosemite)

(ii) Java Runtime Environment Version 7 update 6 or above

(4) Filling the form:

(i) The electronic utility have the following menu options

For first time filing, use lower menu bar. The top menu bar can be used to open a a saved file, save a draft and generate xml after validation.

(ii) Steps involved:

Step-1: Form 15G/H(Consolidated) -> Fill TAN and select the applicable quarter and financial year for which the declaration is to be given.

Step-2: Basic Details -> Fill 10 alphanumeric Unique Identification No. starting with G (for Form 15G) and starting with H (for Form 15H) followed by 9 digits followed by financial year and TAN, then fill details of the assessee (PAN/name, address etc.). Date on which declaration was received. Number of declarations received. Date when income was paid/credited.

Step-3: Income details ->Fill details of income paid or credited, identification number/account, section under which tax is deductible etc.

(5) File validation and generating XML

After filling the form click on "validate" button on the top menu bar. All validation errors shall be displayed at the right hand side blue box. correct the errors and after validation test is passed, click on "Generate XML" and save the file.

(6) DSC is Mandatory to file FORM 15G/15H. Generate signature for the zip file using DSC Management Utility which is available under Downloads tab at income tax efiling website

(7) Login at incometax efiling website through TAN registered, Go to e-File -> Upload Form 15G/15H

(8) Upload the "Zip" file along with the signature file.

(C) Filing Status:

To view the status of the uploaded form 15G/15H files, Go to My account -> View Form 15G/15H.

Once uploaded the status of the statement shall normally be "Uploaded". The uploaded file shall be processed and validated. Upon validation the status shall be either "Accepted" or "Rejected" which will reflect within 24 hours from the time of upload.

Accepted statements shall be sent to CPC-TDS for further processing. In case if "Rejected", the rejection reason shall be available and the corrected statement can be uploaded.

(D) List of validations:

List of various validations carried out on the uploaded statements before they are accepted or rejected are as under:

- Schema validations – uploaded xml should comply with the published schema

- Other Business Validations –

- Only one original will be accepted for combination of TAN, Financial Year, Form and quarter.

- TAN, Filing Type, Quarter and Financial Year entered in XML should match with the TAN, Quarter, Financial Year and Filing Type in upload screen.

- UIN should be unique for the TAN and financial year

- Financial year and TAN in the UIN should match with the TAN and Financial Year for which the statement is being uploaded.

21 March 2016

CBDT on Coercive Recovery of TDS

CBDT Bars Coercive Recovery Of TDS From Payee Even If Payer Has Defaulted By Non-Deposit Of TDS With Govt

The CBDT has issued Office Memorandum dated 11.03.2016 by which it has drawn attention to its earlier letter dated 01.06.2015 in which it was stated that in case of an assessee whose tax has been deducted at source but not deposited to the Government's account by the deductor, the deductee assessee shall not be called upon to pay the demand to the extent tax has been deducted from his income. It was further specified that section 205 of the Income-tax Act, 1961 puts a bar on direct demand against the assessee in such cases and the demand on account of tax credit mismatch in such situations cannot be enforced coercively. The CBDT has noted that instances have come to the notice of the Board that these directions are not being strictly followed by the field officers. The CBDT has accordingly reiterated the instructions contained in its letter dated 01.06.2015 and directed the assessing officers not to enforce demands created on account of mismatch of credit due to non-payment of TDS amount to the credit of the Government by the deductor

Real Estate Regulation-Role of CAs'

Real Estate (Regulation and Development) Act, 2016-Role of Chartered Accountants

Real Estate (Regulation and Development) Act, 2016 has been passed by the Lok Sabha on 15/03/2018. The Bill seeks to streamline and regulate the real estate project working by incorporating various measures to safeguard general public by prescribing adequate procedures and penal provisions.

Recognising the skills of the Chartered Accountants, they have been given due importance and role in the Bill towards protecting the misapplication of the deposits by the promoters.

Role of Chartered Accountants

Amounts from the separate account maintained for deposit of amounts received from allottees shall be withdrawn by the promoter after it is certified by an engineer, an architect and chartered accountant in practice that the withdrawal is in proportion to the percentage of completion of the project.

Also the promoter shall get his accounts audited within six months after the end of every financial year by a chartered accountant in practice, and shall produce a statement of accounts duly certified and signed by such chartered accountant. During the audit it shall be verified that the amounts collected for a particular project have been utilised for the project and the withdrawal has been in compliance with the proportion to the percentage of completion of the project.

Also Chartered Accountants can be appointed as legal representative by the promotor to present him or its case before the Appellate Tribunal or the Regulatory Authority.

Real Estate (Regulation and Development) Act, 2016 Key Highlights

Prior registration of real estate project with Real Estate Regulatory Authority.

Before advertising, booking, selling or inviting persons to purchase any plot, apartment or building etc. in any real estate project registration of the real estate project with the Real Estate Regulatory Authority is must. Ongoing projects to make an application for registration within a period of three months.

However Registration not required:—where the area of land proposed to be developed does not exceed five hundred square meters or the number of apartments proposed does not exceed 8 (eight) inclusive of all phases. Also registration is not required for new allotment or renovation, repair or re-development not involving marketing, advertising.

Registration shall be granted within 30 days and if the prescribed Authority fails to grant the registration or reject the application, the project shall be deemed to have been registered.

Display of project details for public viewing

A web based online system for submitting application for registration of projects shall be developed. The promoter upon registaration shall be given a ogin Id and password to create his web page on the website of the Authority and give all details of the proposed project for public viewing,

Application for registration of real estate project.

Application shall be made in prescribed form with prescribed fee and shall include details of promoters, projects launched in past five years, approval letters/certificates to commence project, lay out plan, allotment letter, agreement for sale proforma , garage, declaration to legal title etc.

Handling with money received from allottees

Application for registration shall be accompinied by a declaration stating that 70% of the amounts realised for the real estate project shall be deposited in a separate account to be maintained in a scheduled bank to cover the cost of construction and the land cost and shall be used only for that purpose.

Registration of real estate agents.

No real estate agent shall be able to facilitate the sale or purchase in a real estate project registered without obtaining registration under new Act. The registration shall be given by the Authority for the entire State/Union territory.

False advertisement or prospectus

If a person makes an advance or a deposit on the basis of false information in advertisement or prospectus, or on the basis of any model apartment, plot or building, and sustains any loss or damage by reason of any incorrect, false statement he shall be compensated and if he intends to withdraw from the proposed project, the promoter shall return his entire investment along with interest at prescribed rates.

No deposit/advance without first entering into agreement for sale and its registration.

A promoter shall not accept more than ten per cent of the cost of the apartment, plot, or building etc. as an advance payment or an application fee, without first entering into a written agreement for sale with such person and register the said agreement for sale.

Insurance of real estate project

The promoter to obtain all specified insurances which shall stand transferred to the benefit of the allottee or the association of allottees, as the case may be, at the time of promoter entering into an agreement for sale with the allottee.

Return of amount and compensation for delay

If the promoter fails to complete or is unable to give possession within scheduled time, he shall in case allottee wishes to withdraw from the project, return the amount with interest at prescribed rates. For those allottee who do not wish to withdraw, the promoter shall pay interest for every month of delay, till the handing over of the possession.

Rights of allottees

- to obtain the information relating to sanctioned plans layout plans along with the specifications

- to know stage-wise time schedule of completion of the project

Real Estate Appellate Tribunal

Appellate Tribunal to be formed within one year. The Tribunal shall not be bound by the procedure laid down by the Code of Civil Procedure, 1908 but shall be guided by the principles of natural justice. Also it shall not be bound by the rules of evidence contained in the Indian Evidence Act, 1872. However, the Tribunal shall for the purpose of discharging its functions shall have the same powers as are vested in a civil court under the Code of Civil Procedure, 1908.

Offences and Penal Provisions for Promoters/real Estate Agents

All offences by promoters/real estate agents against the requirements of the Act, order of the Prescribed Authority, Tribunal etc. have been made punishable with fine, penalty in addition to 3 years maximum imprisonment.

Offences and Penal Provisions for Allottees

Any allottee failing or contravening the orders, directions of the Applellate Tribunal, shall be punishable with imprisonment for a term which may extend upto one year or with fine for every day during which such default continues, which may cumulatively extend up to ten per cent. of the plot, apartment or building cost, as the case may be, or with both

Compounding of punishment with imprisonment

However, any punishment with imprisonment may, either before or after the institution of the prosecution, be compounded by the court on such terms and conditions and on payment of such sums as may be prescribed.

10 key takeaways from Companies Amendment Bill, 2016. Analysis on Companies Amendment Bill,2016

Companies Amendment Bill, 2016 (the bill) was introduced in Lok Sabha on 16th March, 2016. Most of the amendments proposed in bill are broadly aimed at addressing difficulties in implementation of provisions of Companies Act, 2013.

Key amendments proposed in the bill are as follows:

1) Appointment of auditors: It has been proposed to do away with the requirements of annual ratification by members with respect to appointment of auditors. Further, under the exisitng provisions, the auditor who has resigned from the company needs to file Form No. ADT-3 with the company and ROC. His failure to do so may attract maximum penalty of Rs 5 lakhs. Now it has been proposed to reduce such penalty to Rs 50,000. However, such penalty should not exceed the remuneration of auditor.

2) Prohibition on loan or guarantee: Bill seeks to limit the prohibition on loans, advances, etc., to any person in which any of the director is interested in. It has been proposed to allow companies to give loan's or guarantee's or provide security to any person in whom any of the director is interested in subject to passing of special resolution by the company and utilisation of loans by the borrower for its principal business activities.

3) Restrictions on layers of investment companies: Under the existing provisions a company shall make investment through not more than two layers of investment companies. The Bill proposes to delete the restrictions on layers of investments.

4) Managerial remuneration: It has been proposed to do away with requirement of obtaining special resolution and approval of Central Govt. for payment of managerial remuneration in excess of prescribed limits of Schedule V. However, for making such payments prior approval of bank or public financial institution or non-convertible debenture holder or secured creditor is also required before taking approval from shareholders.

5) DIN: It has been proposed to recognise any other identification number, as may be prescribed, in place of DIN.

6) Repayment of deposit: Under the exising provisions, pubic deposits shall be repaid within one year from commencement of the Companies Act, 2013 or from due date of payment, whichever is earlier. Now the bill proposes to provide that such public deposits shall be repaid within 3 years from the enforcement of Section 74 (Repayment of deposit etc., accepted before commencement of the Act) of the Companies Act, 2013 or before expiry of the period for which deposits were accepted, whichever is earlier.

7) Simplification of private placement: Bill proposes to simplify the requirements with reference to private placements, such as doing away with separate offer letter, reducing number of filings with registrar.

8) Liberty on public issue: Bill proposes to remove the restriction which requires company to make issue only after one year has elapsed from the date of commencement of its business.

9) Annual Return: Bill proposes to remove the extract of annual return forming part of Board's report and provide disclosure of web address/web-link of the annual return in Board's report. It also proposes to omit requirement regarding disclosure of indebtedness, and modify requirement of disclosure of names, addresses, countries of incorporation, registration and percentage of shareholding of Foreign Institutional Investors.

10) Maintenance of registered office: Under the existing provisions, the company has to maintain its registered office within 15 days of its incorporation. The bill proposed to provide that a company to has to maintain its registered office within 30 days of incorporation.

09 March 2016

100 % income tax deduction of profits of eligible affordable housing project: Detailed provisions

100 % income tax deduction of profits of eligible affordable housing project: Detailed provisions

With effect from

the FY 2016-17

‘80-IBA. (1) Where the gross total income of an assessee includes any profits and gains derived from the business of developing and building housing projects, there shall, subject to the provisions of this section, be allowed, a deduction of an amount equal to hundred per cent. of the profits and gains derived from such business.

(2) For the purposes of sub-section (1), a housing project shall be a project which fulfils the following conditions, namely:—

(a) the project is approved by the competent authority after the 1st day of June, 2016, but on or before the 31st day of March, 2019, in accordance with such guidelines as may be prescribed;

(b) the project is completed within a period of three years from the date of approval by the competent authority:

Provided that,—

(i) where the approval in respect of a housing project is obtained more than once, the project shall be deemed to have been approved on the date on which the project was first approved by the competent authority; and

(ii) the project shall be deemed to have been completed when a certificate of completion of project as a whole is obtained in writing from the competent authority;

(c) the built-up area of the shops and other commercial establishments included in the housing project does not exceed three per cent. of the aggregate built-up area;

(d) the project is on a plot of land measuring not less than one thousand square meters where such project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or two thousand square meters

within the jurisdiction of any other municipality or cantonment board;

(e) the residential units comprised in the housing project does not exceed thirty square meters where such project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or sixty square meters, where such project is located within the jurisdiction of any other municipality or cantonment board;

(f) where a residential unit in the housing project is allotted to an individual, no other residential unit in the housing project shall be allotted to the individual or the spouse or the minor children of such individual;

(g) the project utilises—

(i) not less than ninety per cent. of the floor area ratio permissible in respect of the plot of land under the rules to be made by the Central Government or the State Government or the local authority, as the case may be, where the project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or

(ii) not less than eighty per cent. of such floor area ratio where such project is located in any area other than the areas referred to in sub-clause (i); and

(h) the assessee maintains separate books of account in respect of the housing project.

(3) Nothing contained in this section shall apply to any undertaking which executes the housing project as a works-contract awarded by any person (including the Central Government or the State Government).

(4) Where the housing project is not completed within the period specified under clause (b) of sub-section (2) and in respect of which a deduction has been claimed and allowed under this section, the total amount of deduction so claimed and allowed in one or more previous years, shall be deemed to be the income of the assessee chargeable under the head “Profits and gains of business

or profession” of the previous year in which the period for completion so expires.

(5) Where any amount of profits and gains derived from the business of developing and building housing projects under any scheme for the housing is claimed and allowed under this section for any assessment year, deduction to the extent of such profit and gains shall not be allowed under any other provisions of this Act.

(6) For the purposes of this section,—

(a) “built-up area” means the inner measurements of the residential unit at the floor level, including projections and balconies, as increased by the thickness of the walls, but does not include the common areas shared with other residential units, including any open terrace so shared;

(b) “competent authority” means the authority empowered by the Central Government;

(c) “floor area ratio” means the quotient obtained by dividing the total covered area of plinth area on all the floors by the area of the plot of land;

(d) “housing project” means a project consisting predominantly of dwelling units with such other facilities and amenities as the competent authority may specify subject to the provisions of this section;

(e) “residential unit” means an independent housing unit with separate facilities for living, cooking and sanitary requirements, distinctly separated from other residential units within the building, which is directly accessible from an outer door or through and interior door in a shared hallway and not by walking through the living space of another household.

With effect from

the FY 2016-17

‘80-IBA. (1) Where the gross total income of an assessee includes any profits and gains derived from the business of developing and building housing projects, there shall, subject to the provisions of this section, be allowed, a deduction of an amount equal to hundred per cent. of the profits and gains derived from such business.

(2) For the purposes of sub-section (1), a housing project shall be a project which fulfils the following conditions, namely:—

(a) the project is approved by the competent authority after the 1st day of June, 2016, but on or before the 31st day of March, 2019, in accordance with such guidelines as may be prescribed;

(b) the project is completed within a period of three years from the date of approval by the competent authority:

Provided that,—

(i) where the approval in respect of a housing project is obtained more than once, the project shall be deemed to have been approved on the date on which the project was first approved by the competent authority; and

(ii) the project shall be deemed to have been completed when a certificate of completion of project as a whole is obtained in writing from the competent authority;

(c) the built-up area of the shops and other commercial establishments included in the housing project does not exceed three per cent. of the aggregate built-up area;

(d) the project is on a plot of land measuring not less than one thousand square meters where such project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or two thousand square meters

within the jurisdiction of any other municipality or cantonment board;

(e) the residential units comprised in the housing project does not exceed thirty square meters where such project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or sixty square meters, where such project is located within the jurisdiction of any other municipality or cantonment board;

(f) where a residential unit in the housing project is allotted to an individual, no other residential unit in the housing project shall be allotted to the individual or the spouse or the minor children of such individual;

(g) the project utilises—

(i) not less than ninety per cent. of the floor area ratio permissible in respect of the plot of land under the rules to be made by the Central Government or the State Government or the local authority, as the case may be, where the project is located within the cities of Chennai, Delhi, Kolkata or Mumbai or within the area of twenty-five kilometers from the municipal limits of these cities, or

(ii) not less than eighty per cent. of such floor area ratio where such project is located in any area other than the areas referred to in sub-clause (i); and

(h) the assessee maintains separate books of account in respect of the housing project.

(3) Nothing contained in this section shall apply to any undertaking which executes the housing project as a works-contract awarded by any person (including the Central Government or the State Government).

(4) Where the housing project is not completed within the period specified under clause (b) of sub-section (2) and in respect of which a deduction has been claimed and allowed under this section, the total amount of deduction so claimed and allowed in one or more previous years, shall be deemed to be the income of the assessee chargeable under the head “Profits and gains of business

or profession” of the previous year in which the period for completion so expires.

(5) Where any amount of profits and gains derived from the business of developing and building housing projects under any scheme for the housing is claimed and allowed under this section for any assessment year, deduction to the extent of such profit and gains shall not be allowed under any other provisions of this Act.

(6) For the purposes of this section,—

(a) “built-up area” means the inner measurements of the residential unit at the floor level, including projections and balconies, as increased by the thickness of the walls, but does not include the common areas shared with other residential units, including any open terrace so shared;

(b) “competent authority” means the authority empowered by the Central Government;

(c) “floor area ratio” means the quotient obtained by dividing the total covered area of plinth area on all the floors by the area of the plot of land;

(d) “housing project” means a project consisting predominantly of dwelling units with such other facilities and amenities as the competent authority may specify subject to the provisions of this section;

(e) “residential unit” means an independent housing unit with separate facilities for living, cooking and sanitary requirements, distinctly separated from other residential units within the building, which is directly accessible from an outer door or through and interior door in a shared hallway and not by walking through the living space of another household.

08 March 2016

CBDT on stay of demand

Analysing CBDT's Office memorandum dated 29.02.2016 regarding stay of demand

Reference to the relevant paragraph in the Union Budget Speech 2016

|

Paragraph 169 of the Union Budget 2016

"The Income-tax Department is also issuing instruction making it mandatory for the assessing officer to grant stay of demand once the assesse pays 15% of the disputed demand, while the appeal is pending before Commissioner of Income-tax (Appeals). In case of deviation, assessing officer has to get orders of his superiors. The tax payer also has an option to go to superior officer in case he does not agree with conditions of stay order passed by the subordinate officer."

|

Reference to the present office memorandum

|

F.No.404/72/93-ITCC dated 29.02.2016

|

Why this new office memorandum?

|

For partial modification of Instruction No. 1914 dated 21.03.1996 to provide for guidelines for stay of demand at the first appeal stage

|

What is the existing provision in Instruction No. 1914 dated 21.03.1996 on the subject?

|

Ref: part 'C'of the Instruction

• A demand will be stayed only if there are valid reasons for doing so

• Mere filing of an appeal against the assessment order will not be a sufficient reason to stay the demand.

• While granting stay, the Assessing officers (AO) may require the assessee to offer a suitable security (bank guarantee, etc.) and/ or require the assessee to pay a reasonable amount in lump sum or in installments.

|

What is the hardship faced by assessees at present

|

AOs often insist on payment of a very high proportion of the disputed demand before granting stay of the balance demand. This often results in hardship for the taxpayers seeking stay of demand.

|

What is sought to be achieved through this new office memorandum?

|

To streamline and standardize the quantification of the 'lumpsum amount' to be paid by the assessee in order to grant stay of the balance amount by the AO

|

What are the new conditions vis-à-vis grant of stay?

|

• the outstanding demand shall be disputed before CIT (A)

• the AO shall grant stay of demand till disposal of first appeal on payment of 15% of the disputed demand

• Subject to the two exceptions that are listed below

|

Exception 1 – AO can demand payment of a sum higher that 15%

|

If the AO is of the view that the nature of addition resulting in the disputed demand is such that payment of a lump sum amount higher than 15% is warranted (e.g. in a case where addition on the same issue has been confirmed by appellate authorities in earlier years or the decision of the Supreme Court /or jurisdictional High Court is in favour of Revenue or addition is based on credible evidence collected in a search or survey operation, etc.) or,

|

Exception 2 – AO can permit payment of a sum lower that 15%

|

If the AO is of the view that the nature of addition resulting in the disputed demand is such that payment of a lump sum amount lower than 15% is warranted (e.g. in a case where addition on the same issue has been deleted by appellate authorities in earlier years or the decision of the Supreme Court or jurisdictional High Court is in favour of the assessee, etc.)

|

What should the AO do in cases of Exception 1 or Exception 2?

|

The AO shall refer the matter to the administrative Pr. CIT/ CIT, who after considering all relevant facts shall decide the quantum/ proportion of demand to be paid by the assessee as lump sum payment for granting a stay of the balance demand.

|

The AO grants stay of demand after payment of 15% of disputed tax by assessee and if the assessee is still aggrieved, what shall he do?

|

The assessee can approach the jurisdictional administrative Pr. CIT/ CIT for a review of the decision of the assessing officer.

|

Time limit for disposing off the stay application by AO

|

The AO shall dispose of a stay petition within 2 weeks of filing of the petition

|

Time limit before PrCIT or CIT of disposing off AO's reference application or assessee's review application

|

The same shall be disposed of by the Pr. CIT/ CIT within 2 weeks of the assessing officer making such reference or the assessee filing such review, as the case may be.

|

Conditions that can be imposed by the AO for granting stay of demand

|

The AO may impose such conditions as he may think fit. He may, inter alia

• require an undertaking from the assessee that he will cooperate in the early disposal of appeal failing which the stay order will be cancelled;

• reserve the right to review the order passed after expiry of reasonable period (say 6 months) or if the assessee has not cooperated in the early disposal of appeal, or where a subsequent pronouncement by a higher appellate authority or court alters the above situations;

• reserve the right to adjust refunds arising, if any, against the demand, to the extent of the amount required for granting stay and subject to the provisions of section 245.

|

Effective date

|

Immediate effect from 29.02.2016

|

CA PRASANTH

e Form 35

CBDT notifies new Form for e-filing of appeal before CIT(A)

INCOME-TAX (THIRD AMENDMENT) RULES, 2016 - SUBSTITUTION OF RULE 45 AND FORM NO.35

NOTIFICATION NO. SO 637(E) [NO.11/2016 (F.NO.149/150/2015-TPL)], DATED 1-3-2016

In exercise of the powers conferred by sub-section (1) of section 249, read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:—

1. (1) These rules may be called the Income-tax (3rd Amendment) Rules, 2016.

(2) They shall come into force on the date of their publication in the Official Gazette.

2. In the Income-tax Rules, 1962 (herein after referred to as the said rules), for rule 45, the following rule shall be substituted, namely:-

"45. Form of appeal to Commissioner (Appeals).—(1) An appeal to the Commissioner (Appeals) shall be made in Form No. 35.

(2) Form No. 35 shall be furnished in the following manner, namely:—

| (a) | in the case of a person who is required to furnish return of income electronically under sub-rule(3) of rule 12,— |

| (i) | by furnishing the form electronically under digital signature, if the return of income is furnished under digital signature; | |

| (ii) | by furnishing the form electronically through electronic verification code in a case not covered under sub-clause (i); |

| (b) | in a case where the assessee has the option to furnish the return of income in paper form, by furnishing the form electronically in accordance with clause (a) of sub- rule(2) or in paper form. |

(3) The form of appeal referred to in sub-rule (1), shall be verified by the person who is authorised to verify the return of income under section 140 of the Act, as applicable to the assessee.

(4) Any document accompanying Form No. 35 shall be furnished in the manner in which the said form is furnished.

(5) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall—

| (i) | specify the procedure for electronic filing of Form No.35 and documents; | |

| (ii) | specify the data structure, standards and manner of generation of electronic verification code, referred to in sub-rule(2), for the purpose of verification of the person furnishing the said form; and | |

| (iii) | be responsible for formulating and implementing appropriate security, archival and retrieval of policies in relation to the said form so furnished." |

3. In the said rules, in Appendix-II, for Form No.35, the following form shall be substituted, namely:—

|

(See rule 45)

Appeal to the Commissioner of Income-tax (Appeals)

|

Subscribe to:

Posts (Atom)

-

*1. What is Pradhan Mantri Garib Kalyan Deposit Scheme (PMGKDS), 2016?* Pradhan Mantri Garib Kalyan Deposit Scheme (PMGKDS), 2016 is a sche...

-

After the ICAI regional council and central council elections , there is an anxious waiting period for resul...

-

Gentlemen: AmtInWords.xla is attached to this mail. It is an MS Excel Add-in written by me to convert amount available in figures to words. ...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}