Now the count down. The real numbers. What we see is guesses. And this all will answer the questions...

1. Can Gujarat give 3 CCM?

2. Can Julfesh Shah make it?

3. Who will be in Dhiraj Khandelwal or BM Agarwal

Summary of the moves for the Extention of Date u/s 44AB:-

1.Bombay HC-Chamber of Tax Consultants Vs. Union of India & Ors (WP-2764/2015)

Adjourned to 29-09-2015

2. Orissa HC-Jagdish Prasad Mittal Vs. Union of India & Ors

WP-17178/2015

Adjourned to 25-09-2015

3. Karnataka HC-Karnataka State Chartered Accountants Association (KSCAA) Vs. Union of India & Ors

WP-41109/2015

Judgment on 28-09-2015

4. Rajasthan HC-Devendra Kumar Somani Vs. Union of India & Ors

(CW-10974/2015)

Now Listed on 29-09-2015

5.Delhi HC- Avinash Gupta & Ors. Vs. Union of India & Ors

(WP(C)-9032/2015)

Extension Refused :21-09-2015

6. Punjab & Haryana HC-Vishal Garg & Ors. Vs. Union of India & Anr (CWP-19770/2015)

Next Hearing : 28-09-2015

7.Gujarat HC-All Gujarat Federation of Tax Consultants (AGFTC) vs Central Board of Direct Taxes ( SCA-15075/2015)

Next hearing 28-09-2015.

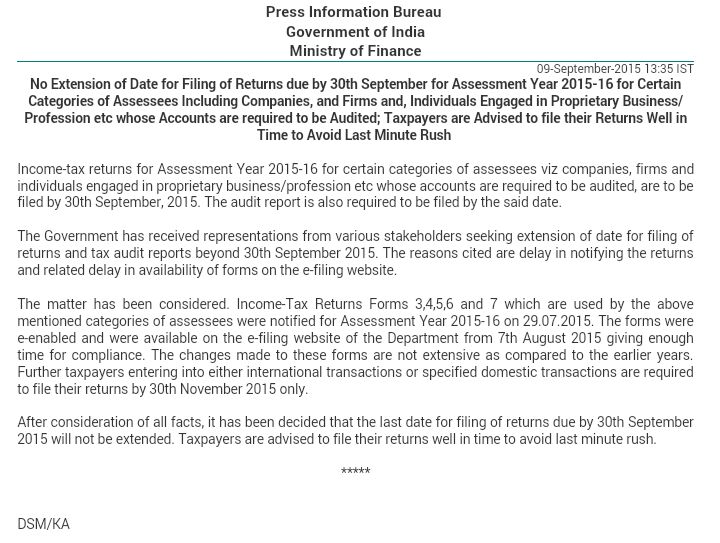

HC dismisses petition filed by Chartered Accountant seeking extension of tax audit due date; Petitioner argued that assessees are entitled as a matter of 'right', to 180 days period for filing of return which in the instant case was being denied since the forms were notified only on July 29, 2015; Petitioner further justified extension plea on grounds of amendments in Companies Act, bonafide impression among CAs that there would be changes/modifications in Form 3CD due to Finance Act amendments and alleged discrimination by CBDT through its act of granting extension for July 31st due date but refusing to do the same for tax audit; HC, rejecting petitioner's submissions, observes that nowhere in the scheme of Income tax Act is 180 days assured to the assessee, holds".. the time taken in audit, which is variable, will be determinative of the time available thereafter for filing the ITR. The said audit is not dependent upon the prescription of the forms for report of the said audit and / or for filing of the ITR. " ; HC notes that the CBDT has applied its mind in the matter, cites its press release dated September 9 ruling out any extension of due date; Further rules that such policy decisions of Government ought not to be interfered by the Court, unless undue prejudice caused; However Court directs CBDT to ensure that the forms that are to be prescribed for the Audit Report/for filing ITR, are available as on April 1 of the assessment year unless there is a valid reason that ought to be recorded :Delhi High Court

1.Anything which you cannot do directly that you cannot do directly

2.Deeming fiction cannot be stretched beyonyd the purpose for which it is created

3.The words used in Law are not used for Nothing

4.To invoke Provision : To make use of particular provision

5.Ipso Facto: By this fact alone or because of this matter alone

6.'MAY' may be treated as 'SHALL' but 'SHALL' shall not be treated as 'MAY'

7.Tenable: Acceptable in law

8.Redundant Provision : Out of Force or Outdated Provision

9.Quasi : Almost Similar to

10.Quasi Criminal: Almost equal to criminal

11.Jurisprudence: Law relating to particular matter

12.Mensrea: Guilty Mind

13.Ibid: As printed earlier

14.Suo Moto: On its own

15.Prima Facie: On its face

16.Non est: What is not in existence / Non existing thing

17.Call in question: To challenge

18.De Nova: Completely New

19.Sine quo non: Most essential thing

20.Purposes of this Act: Proceeding mustbe pending

21.Reason to believe Vs Reason to suspect: Refer various caselaws

22.Derived from & attributable to: Derived from refers to direct connection with aparticular matter whereas attributable to refers to an indirect connection

23.Mutatis Mutandis: After making necessary changes as may be required

24.Discovery Vs Detection: Discovery is made by the assessee whereas detectionisdone by the Assessing Officer

25.To Quash: The process of cancelling the proceeding of Assessing Authorities byJudicial Authorities

26.So far as may be: To the extent possible

27.Travisity of Justice : A ridiculous interpretation of a very serious statement,making amockery of a very serious matter

28.To impugne : To challenge

29.Save as otherwise provided : Except tothe extent as oppositely provided

30.If one section is overriding the other section : Use Words "Not withstandinganything contained in ……

"31.If one section is superceded by the other section : Use words "Save as otherwiseprovided……….."32.Other provisions apply in General way:Use words "Without prejudice to theprovisions ……………..

"33.Reckoned : Recognised, Counted, Calculated

34.Doctrine of Merger: When an order passed by the lower authority is superceded bythe higher authority

35.Doctrine : Principle or saying in general acceptance

36.In Pari Material Pavi Causa: Same material, same content {Eg. Sec. 24B of ITAct,1922 is Pari Material with Sec. 159 of IT Act, 1961. In such a case a judgement givenin respect of section 24B would be valid in respect of sec. 159}

37.Per se : By itself

38.Cy Press : As near as possible

39.Tax is always charged, Interest is levied and Penalty is imposed40 Deductions are admissible, Relief is granted.

41.Return is always furnished, Assessment order is made / passed.

42.De hors : Independent of

43.Order of Injunction of HC : Stay order.

44.Several Liability means separate liability. [Refer sections 168(3), 171(7), 179(1)178(5) & 188A.]

45.Legatee is a person for whose benefit there exists an asset of a deceased

46.Locus Standi : Directly involved in relation or deal.

47.Garnishee Proceeding : The proceeding which gives Govt. the right to attach (i.e.forcibly take over) any asset from a person who is defaulter.

48.Vitiate Proceedings : To make proceedings null, void.

49.Inter alia : Among other things.

50.Audit Altream partem : It is a principle of natural justice. According to this principle,which is the principle in every civilized jurisprudence, a person against whom anyaction is sought to be taken or a person whose rights or interests are to be affectedshould be given a reasonable opportunityto defend himself.

51.Resjudicata : [Once the decision of HC comes then on that same point again appealcannot be made.] The issue of Law whichhas been already decided shall not bepleaded for review.

52.In Limine : At the outset (i.e. at the beginning)

53.Suspended animus : An order under Appeal is not subject to any action by anyauthority till the order disposing of the appeal is available.

54.Subjudice : Under an appeal to a court,decision awaited.

55.Adjudicate : Consider for judgement. Acourt adjudicates means gives its decision ona particular matter.

56. Akin : Similar to; of the same typeCoterminus : Similar to; of the same type

57.Impediment : Obstacles or Hindrance.

58.Sine Di: For indefinite period.

59. To deduce : Logically come to the conclusion.

60.Purview : Scope

61.Bounty : Additional Advantage

62.Ad Hoc : Without any particular rate, percentage, proportion.

63.Ad infinitum : Without any Time limit.

64.Ad interim : In the Mean Time

65.Bonafide : Genuine

66.Surmises : Presumptions, own assumptions

67.Defacto : Infact

68.Defjure : In Law, irrespective of whatever the facts.

69.Ejusdem Generis : Of the same kind

70.Ex-gratia : As a matter of grace ir favour

71.Ignorantia Legis known excusat : Ignorance of law is not excused

72.Mesne Profit : Profit earned by somebody by wrongful possession of property.

73.Modus Operandi : Mode of Operation /Manner of working

74.Nexus : Close connection link.

75.Onus probandi : Onus of proof / The burden of Proof.

76.Non obnstante clause : That provisionhas superceding effect on any other provision

77. Raison D'etre : Reason or justification for existence.

78.Ratio Decidendi : Reason for deciding / Grounds for decision

79.Suijuris : of his own right.

80.Assessee engaged in ……………. : The activity should have started

81.Option Vs Discretion : Whenever choices is available to the assessee in respect ofany matter. Law uses the word at his option - for eg:1. Sec 11(11) - Explanation to Sec. 11 (1)2. Sec. 23(4)

82.amicus curiae : Friend of court; one who voluntarily or on invitation of the court, andnot on instructions of any party, helps thecourt in any judicial proceedings

83.audi alteram : hear the other side. Both sides should be heard before a decision isarrived at

84.caveat emptor : let the purchaser beware. A ---------- implying that the buyer mustbe cautious, as the risk is his and not thatof the seller.

85.cestui que trust : a beneficiary under atrust, the person for whose benefit the trust iscreated

86.ex officio : by virtue of an office.

87.ex parte : exkpression used to signify something done or said by one person not in thepresence of his opponent.

88.fait accompli : An accomplished act.

89.obiter diccum : an opinion of law not necessary to the decision. An exspression ofopinion (formed) by a judge on a question immaterial to the ratio decidendi, andunnecessary for the decision of the particular case. It is no way binding on any court,but may receive attention as being an opinion of the high authority.

90.pendente lite : during litigation.

91. per incuriam : through carelessness, through inadvertence. A decision of the court isnot binding precedent if given peer incuriam, that is, without the court's attention havingbeen drawn to the relevant authorities, or statutes.

92. pro tanto : to that extent, for so much, for as much as may be.

93. quid pro quo : the giving of one thing of value for another thing of value; one fortheother; thing given as compensation.

94. Ratio Decidendi : Reason for deciding / Grounds for decision

95. res integra : an untouched matter; a point without a precedent; a case of novelimpression.

96 rule njsi : a rule to show cause why a party should not do a certain act, or why theobject of the rule should not be enforced.

97 in personam : against the person; an act or preceeding done or directed withreference to no specific person or with reference to all whom it might concern.

98 in rem : an act / proceeding done or directed with reference to no specific person orwith refernce to all whom it might concern.

99 inter vivos : between living persons.

100 intestate : a person is deemed to die intestate in respect of property of which he or shehas not made a testamentary disposition ("will") capable of taking effect.

101 intra vires : within the powers; within the authority given by law.

102 ipse dixit : he himself said it; there is no other authority.

103 ipso jure : by the law itself ; by the mere operation of law.

104 lis pendens : a pending suit.

105 rule absolute : when, having heard counsels, court directs the performance of that actforthwith.

106 sine die : without delay.

107 stare decisis : to stand by things decided; to abide by precedents where the samepoints come again in litigation.

108 status quo : existing condition.

109 sub judice : before a judge or court; pending decision of a competent court.

110 ultra vires : beyond one's power..

1.Anything which you cannot do directly that you cannot do directly

2.Deeming fiction cannot be stretched beyonyd the purpose for which it is created

3.The words used in Law are not used for Nothing

4.To invoke Provision : To make use of particular provision

5.Ipso Facto: By this fact alone or because of this matter alone

6.'MAY' may be treated as 'SHALL' but 'SHALL' shall not be treated as 'MAY'

7.Tenable: Acceptable in law

8.Redundant Provision : Out of Force or Outdated Provision

9.Quasi : Almost Similar to

10.Quasi Criminal: Almost equal to criminal

11.Jurisprudence: Law relating to particular matter

12.Mensrea: Guilty Mind

13.Ibid: As printed earlier

14.Suo Moto: On its own

15.Prima Facie: On its face

16.Non est: What is not in existence / Non existing thing

17.Call in question: To challenge

18.De Nova: Completely New

19.Sine quo non: Most essential thing

20.Purposes of this Act: Proceeding mustbe pending

21.Reason to believe Vs Reason to suspect: Refer various caselaws

22.Derived from & attributable to: Derived from refers to direct connection with aparticular matter whereas attributable to refers to an indirect connection

23.Mutatis Mutandis: After making necessary changes as may be required

24.Discovery Vs Detection: Discovery is made by the assessee whereas detectionisdone by the Assessing Officer

25.To Quash: The process of cancelling the proceeding of Assessing Authorities byJudicial Authorities

26.So far as may be: To the extent possible

27.Travisity of Justice : A ridiculous interpretation of a very serious statement,making amockery of a very serious matter

28.To impugne : To challenge

29.Save as otherwise provided : Except tothe extent as oppositely provided

30.If one section is overriding the other section : Use Words "Not withstandinganything contained in ……

"31.If one section is superceded by the other section : Use words "Save as otherwiseprovided……….."32.Other provisions apply in General way:Use words "Without prejudice to theprovisions ……………..

"33.Reckoned : Recognised, Counted, Calculated

34.Doctrine of Merger: When an order passed by the lower authority is superceded bythe higher authority

35.Doctrine : Principle or saying in general acceptance

36.In Pari Material Pavi Causa: Same material, same content {Eg. Sec. 24B of ITAct,1922 is Pari Material with Sec. 159 of IT Act, 1961. In such a case a judgement givenin respect of section 24B would be valid in respect of sec. 159}

37.Per se : By itself

38.Cy Press : As near as possible

39.Tax is always charged, Interest is levied and Penalty is imposed40 Deductions are admissible, Relief is granted.

41.Return is always furnished, Assessment order is made / passed.

42.De hors : Independent of

43.Order of Injunction of HC : Stay order.

44.Several Liability means separate liability. [Refer sections 168(3), 171(7), 179(1)178(5) & 188A.]

45.Legatee is a person for whose benefit there exists an asset of a deceased

46.Locus Standi : Directly involved in relation or deal.

47.Garnishee Proceeding : The proceeding which gives Govt. the right to attach (i.e.forcibly take over) any asset from a person who is defaulter.

48.Vitiate Proceedings : To make proceedings null, void.

49.Inter alia : Among other things.

50.Audit Altream partem : It is a principle of natural justice. According to this principle,which is the principle in every civilized jurisprudence, a person against whom anyaction is sought to be taken or a person whose rights or interests are to be affectedshould be given a reasonable opportunityto defend himself.

51.Resjudicata : [Once the decision of HC comes then on that same point again appealcannot be made.] The issue of Law whichhas been already decided shall not bepleaded for review.

52.In Limine : At the outset (i.e. at the beginning)

53.Suspended animus : An order under Appeal is not subject to any action by anyauthority till the order disposing of the appeal is available.

54.Subjudice : Under an appeal to a court,decision awaited.

55.Adjudicate : Consider for judgement. Acourt adjudicates means gives its decision ona particular matter.

56. Akin : Similar to; of the same typeCoterminus : Similar to; of the same type

57.Impediment : Obstacles or Hindrance.

58.Sine Di: For indefinite period.

59. To deduce : Logically come to the conclusion.

60.Purview : Scope

61.Bounty : Additional Advantage

62.Ad Hoc : Without any particular rate, percentage, proportion.

63.Ad infinitum : Without any Time limit.

64.Ad interim : In the Mean Time

65.Bonafide : Genuine

66.Surmises : Presumptions, own assumptions

67.Defacto : Infact

68.Defjure : In Law, irrespective of whatever the facts.

69.Ejusdem Generis : Of the same kind

70.Ex-gratia : As a matter of grace ir favour

71.Ignorantia Legis known excusat : Ignorance of law is not excused

72.Mesne Profit : Profit earned by somebody by wrongful possession of property.

73.Modus Operandi : Mode of Operation /Manner of working

74.Nexus : Close connection link.

75.Onus probandi : Onus of proof / The burden of Proof.

76.Non obnstante clause : That provisionhas superceding effect on any other provision

77. Raison D'etre : Reason or justification for existence.

78.Ratio Decidendi : Reason for deciding / Grounds for decision

79.Suijuris : of his own right.

80.Assessee engaged in ……………. : The activity should have started

81.Option Vs Discretion : Whenever choices is available to the assessee in respect ofany matter. Law uses the word at his option - for eg:1. Sec 11(11) - Explanation to Sec. 11 (1)2. Sec. 23(4)

82.amicus curiae : Friend of court; one who voluntarily or on invitation of the court, andnot on instructions of any party, helps thecourt in any judicial proceedings

83.audi alteram : hear the other side. Both sides should be heard before a decision isarrived at

84.caveat emptor : let the purchaser beware. A ---------- implying that the buyer mustbe cautious, as the risk is his and not thatof the seller.

85.cestui que trust : a beneficiary under atrust, the person for whose benefit the trust iscreated

86.ex officio : by virtue of an office.

87.ex parte : exkpression used to signify something done or said by one person not in thepresence of his opponent.

88.fait accompli : An accomplished act.

89.obiter diccum : an opinion of law not necessary to the decision. An exspression ofopinion (formed) by a judge on a question immaterial to the ratio decidendi, andunnecessary for the decision of the particular case. It is no way binding on any court,but may receive attention as being an opinion of the high authority.

90.pendente lite : during litigation.

91. per incuriam : through carelessness, through inadvertence. A decision of the court isnot binding precedent if given peer incuriam, that is, without the court's attention havingbeen drawn to the relevant authorities, or statutes.

92. pro tanto : to that extent, for so much, for as much as may be.

93. quid pro quo : the giving of one thing of value for another thing of value; one fortheother; thing given as compensation.

94. Ratio Decidendi : Reason for deciding / Grounds for decision

95. res integra : an untouched matter; a point without a precedent; a case of novelimpression.

96 rule njsi : a rule to show cause why a party should not do a certain act, or why theobject of the rule should not be enforced.

97 in personam : against the person; an act or preceeding done or directed withreference to no specific person or with reference to all whom it might concern.

98 in rem : an act / proceeding done or directed with reference to no specific person orwith refernce to all whom it might concern.

99 inter vivos : between living persons.

100 intestate : a person is deemed to die intestate in respect of property of which he or shehas not made a testamentary disposition ("will") capable of taking effect.

101 intra vires : within the powers; within the authority given by law.

102 ipse dixit : he himself said it; there is no other authority.

103 ipso jure : by the law itself ; by the mere operation of law.

104 lis pendens : a pending suit.

105 rule absolute : when, having heard counsels, court directs the performance of that actforthwith.

106 sine die : without delay.

107 stare decisis : to stand by things decided; to abide by precedents where the samepoints come again in litigation.

108 status quo : existing condition.

109 sub judice : before a judge or court; pending decision of a competent court.

110 ultra vires : beyond one's power..

Sl No.

|

Name

|

Designation

| |

1

|

Ms Sunita Puri

|

Principal Commissioner of Income Tax -IV, Delhi

|

Committee In- charge

|

2

|

Sh. B. K. Singh

|

CIT(A)-11, Delhi

|

Members

|

3

|

Sh. Samar Bhadra

|

ADG (System)-3, Delhi

| |

4

|

Sh Rajeev Ranka

|

Add I. CIT (Audit-1), Delhi

| |

5

|

Sh. Rajesh Kedia

|

Addl CIT, Delhi

| |

6

|

Smt. Garima Bhagat

|

Addl CIT, Delhi

|

Member Secretary

|

The government today approved the Sovereign Gold Bonds Scheme, which was announced in the Budget 2015-16. As investors will get returns that are linked to gold price, the scheme is expected to reduce the demand for physical gold. The bonds will offer same benefits as physical gold.

They can be used as collateral for loans and can be sold or traded on stock exchanges as they are available in demat form. At the same time investors need not worry about holding physical gold.

The gold bonds will be issued by the Reserve Bank of India. Since these are Government of India bonds, they are sovereign.

The bonds will be denominated in grams of gold. Investors can pay money and buy these bonds from intermediaries, who will be announced later.

* The bonds can be purchased only by resident individuals or entities. There will be a cap on bonds that can be purchased. It could be 500 gms per person per year.

* The government will decide the rate of interest. The rate will be calculated on the value of the gold at the time of investment. It could be floating or fixed rate. The principal amount of investment, which is denominated in grams of gold, will be redeemed at the price of gold at that time. If the price of gold has fallen from the time that the investment was made, the depositor will be given an option to roll over the bond for three or more years.

* The bonds will be available both in demat and paper form. They will be issued in denominations of 5,10,50,100 gms of gold or other denominations

* The bonds will be issued and redeemed by banks, non-banking finance companies, National Saving Certificate (NSC) agents for a fee. This fee will be decided later

* The price of gold may be taken from the reference rate, as decided and the rupee equivalent amount may be converted at the RBI reference rate on issue and redemption. This rate will be used for issuance, redemption and Loan to Value purpose and disbursement of loans.

* The tenor of the bond could be for a minimum of five to seven years.

* These bonds can be used as collateral for loans. The LTV will be equal to that of ordinary gold loans. As per RBI regulations, the maximum LTV allowed for gold loans is 75 per cent.

* It will be possible to sell and trade the bonds on exchanges, in case investors want to redeem them before maturity. The KYC for the bonds is same as that for gold. Currently, if you purchase gold worth more than Rs 50,000 you have to show proof of KYC, such as PAN card, etc.

* Capital gains tax will be the same as for physical gold for individual investors. This means that short-term capital gains tax will apply if you sell within three years. The profits will be added to your income and taxed at income slab. Long term capital gains tax is 20 per cent with indexation.

ITAT accedes to ICAI's plea in Miscellaneous Application to modify/review its order wherein the Tribunal had strongly criticized the Institute's functioning; Tribunal accepts ICAI's argument that that its observations in the original order about the CA profession and conduct of the students pursuing the CA courses, were not necessary to adjudicate the issues urged before it by the assessee; Clarifying that it was not the intention of the Tribunal to target any particular person or the ICAI, modifies para 9.6 of its original order that the Institute considered as "offensive"; ITAT in its original order, dismissed assessee's plea to condone a 2984 days delay in filing of appeal on grounds of 'improper advice' given by CA firm; While raising alarms over the reckless advice given by the CA firm, the Tribunal called on the ICAI to stem the"deteriorating standards" & "alarming practices" among some CAs; While modifying its order, Tribunal however reserves right to opine on important developments affecting the nation, observes “... the Income tax Appellate Tribunal, being a part of Government of India, should not shut its eyes when it is noticed that certain developments occurring in the Country may affect the Country as a whole, more particularly when the reputation of particular profession, from whom the Tribunal is getting assistance in the dispensation of justice, is at stake.”; Concludes that it would be incorrect to interpret that the Tribunal in its original order had commented upon the standards of CA profession or the ICAI, however as the said observations gave room for misinterpretation and thereafter resulted in controversies, replaces the same : Mumbai ITAT

The ruling was delivered by ITAT bench of Shri D. Manmohan and Shri B. R. Baskaran.

BCAS in its knowledge sharing mission, interacts with the law makers to bring clear, predictable, just, hassle free laws and good governance. In this endeavour, this month the Society has made 2 representations to the government on various issues and hardships faced by the Chartered Accountants.

a) Representation to CBDT on E-filing of Wealth-Tax Returns, and

b) Representation to the Ministry of Corporate Affairs for The Company Act, 2013 on issues arising from the implementation of the Companies Act, 2013.

We hope that this will help our members and their clients.

Please click on below links to read the full representations :

· Representation to CBDT on E-filing of Wealth-Tax Returns for A.Y. 2015-16

· The Companies Act 2013 - Issues arising from the implementation of the companies act, 2013

Government Accepts Shah Panel Report, MAT Not to be Levied on FIIs

Finance Minister Arun Jaitley on Tuesday announced that the government has accepted Justice AP Shah Panel's recommendations on not levying MAT on Foreign Institutional Investors.

A. Highlights of speech

Here are the highlights of his speech.

B. Recommendations of AP Shah Pane Committee

In view of the findings and upon a considered deliberation, we would like to make the following recommendations to the Government:

(i) To bring an amendment to Section 115JB of the Income Tax Act, 1961 clarifying the complete inapplicability of the MAT provisions to FIIs/FPIs; or

(ii) CBDT may issue a circular clarifying the complete inapplicability of the MAT provisions to FIIs/FPIs.

Criteria for manual selection of scrutiny cases during FY 2015-16

CBDT Instruction No. 8 Dated 31-8-2015

Highlights:

Cases involving addition in excess of Rs. 10 lakhs in earlier assessment year and all search-seizure-survey and re-assessment cases to be picked up for compulsory manual scrutiny.

Cases where charitable trusts/institutions are claiming Sec 11/Sec 10(23C) exemption despite Sec 12AA registration /Sec 10(23C) approval denial also to be picked up for compulsory manual scrutiny.

By and large no substantial changes via-à-vis similar CBDT instruction issued last year.

SEBI issues Guidance Note on Insider Trading Regulations, clarifies on ESOPs & contra-trades

|

SEBI issues Guidance Note on Insider Trading Regulations, 2015; Clarifies that exercise of ESOPs shall not be considered to be "trading" except for the purposes of Chapter III (relating to 'disclosure of trading by insiders'); States that any derivative contract that is settled in cash on expiry shall be considered to be 'contra-trade' and the trading in index futures or such other derivatives where scrip is part of such derivatives, need not be reported; States that buy-back offers, open offers, rights issues, FPOs, bonus are available to designated persons, and 'contra-trade' restrictions shall not apply; Clarifies that pledgor / pledgee may demonstrate that creation of pledge or invocation of pledge was bona fide and prove their innocence under proviso to Reg. 4(1) of the Regulations (relating to 'Trading when in possession of unpublished price sensitive information'); With respect to the trades done by compliance officer, SEBI clarifies that board of directors of the company shall be the approving authority and may stipulate procedures as are deemed necessary for ensuring necessary compliances: SEBI

|

Circular no 14 has been issued by CBDT today pertaining to approval and exemption u/s 10(23c)vi of I.T Act, 1961

The Board of Studies of the institute has great pleasure in introducing an optional Articles Placement Scheme for selection of Articled Assistants by CA Firms. The scheme has been evolved to provide an opportunity to the firms of Chartered Accountants having vacancies for Articled Assistants to interact with the candidates who have either (a) Passed Group-I or both Groups of the IPCC examination , or (b) have been admitted under the Direct Entry Scheme and are eligible for undergoing articled training for selection as articled assistants in the C A Firms. This scheme at the same time, assists eligible students to get placement in CA Firms for their articles training.

No Fee is to be Charged From the Participating CA Firms and Students registering on the Portal.

http://bosapp.icai.org

RBI Credit Policy (04 July 2015): RBI keeps rate unchanged with Repo Rate at 7.25%; Reverse Repo Rate stands at 6.25%; CRR unchanged at 4%. Estimated GDP growth for FY16 @7.60%.

ICAI Announcement (03-08-2015)

Multipurpose Empanelment Form (MEF) for the year 2015-16.

This is to inform that Multipurpose Empanelment Form (MEF) for the year 2015-16 has been made live at www.meficai.org. The Members/firms can apply the form showing the status as on 1st January 2015. After filling the form, they are required to generate an online Declaration and Acknowledgment letter. They are also required to submit hard copy of Declaration in support of their online application along with a print out of the acknowledgment letter generated online. The application which does not have Declaration would not be entertained as a valid application.

Last date for submission of online form is 31st August, 2015 and last date of submission of hard copy of "DECLARATION FOR MEF 2015-16" is 15th September, 2015.

It is suggested that before going directly to the MEF form, applicant should first go through the link http://www.meficai.org/Advisory_2015.pdf "Points which shall be carefully read and be taken care for MEF 2015-16".